If you frequently attend conferences, you might have noticed the term “PayFi.” In fact, it’s a recurring theme in the speeches of Lily Liu, the Chairperson of the Solana Foundation. This article delves into the concept of “PayFi” and related projects to help readers stay updated with the latest narrative surrounding Solana.

What is PayFi?

According to Lily Liu, “The motivation behind PayFi is to fulfill Bitcoin’s original vision for payments. PayFi is not DeFi; instead, it creates new financial primitives centered around the time value of money.”

The Vision of PayFi

Lily Liu’s reference to Bitcoin’s original vision for payments goes beyond the simple idea of a “peer-to-peer electronic financial system.” It extends to “Program Money, Open Financial System, Digital Property Rights, Self Custody, and Economic Sovereignty.” PayFi’s vision is to build a system of programmable money within an open financial system, offering users economic sovereignty and self-custody capabilities.

Programmable money refers to digital currency that can be used not only for traditional transactions and payments but also for executing complex financial operations automatically based on pre-set rules.

While smart contracts and DeFi are applications of programmable money, PayFi is not considered DeFi because DeFi primarily revolves around financial products and trading, whereas PayFi aims to create products centered on goods and services, placing it more accurately within the Real World Asset (RWA) sector.

The Time Value of Money

When discussing PayFi, Lily Liu often mentions three examples: “Buy Now Pay Never,” “Creator Monetization,” and “Account Receivable.” Understanding these examples provides deeper insight into PayFi.

1. Buy Now Pay Never

Most people are familiar with “Buy Now Pay Later” (BNPL), which involves installment payments. However, “Buy Now Pay Never” is almost the opposite of BNPL. BNPL is a form of credit, where one incurs interest costs in exchange for better cash flow.

On the other hand, Buy Now Pay Never involves depositing money into DeFi products, earning interest through lending, and then using that interest to make payments, thus sacrificing cash flow.

For instance, if a user buys a $5 coffee, they would deposit $50 into a lending product. When the interest accumulates to $5, the coffee is paid for, and the remaining funds are unlocked and returned to the user’s account. All of this is executed automatically, requiring the “programmable money” mentioned earlier.

2. Creator Monetization

This example addresses the cash flow difficulties faced by many creators. Creating content requires time and financial investment, but creators often don’t receive immediate compensation after their work is completed, leading to a long wait for payment.

If a creator lacks sufficient cash reserves, they may be unable to continue creating during this waiting period, resulting in wasted time.

In Lily Liu’s vision, PayFi can help creators solve this problem. For example, if a video generates $10,000 in revenue but takes a month to receive, the creator could use PayFi to immediately receive $9,000 by discounting their future earnings, thus improving cash flow by sacrificing a portion of the income.

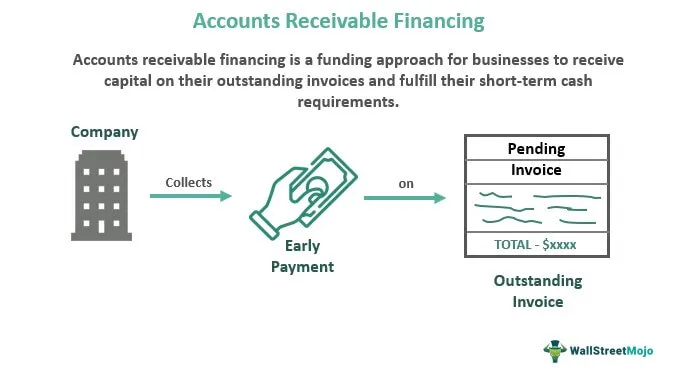

3. Account Receivable

Account receivable is a traditional concept where a company is owed money by its customers. Due to the existence of accounts receivable, companies may encounter cash flow issues. To address this, various receivables financing companies have emerged, allowing businesses to use their accounts receivable as collateral for loans or sell them at a discount to obtain cash immediately. This ensures stable cash flow and continuous growth, regardless of the speed at which customers pay.

PayFi aims to further popularize and optimize this scenario. While such services already exist in Web2, the overall capital turnover still depends on traditional payment systems, leading to slow settlements. If blockchain technology can be used to speed up settlements and make supply chain finance services more accessible, lowering the barriers, the entire real-world capital turnover rate could improve.

4. The Time Value of Money and PayFi’s Potential

All three examples revolve around the “time value of money,” which refers to the idea that due to opportunity costs, interest rates, and other factors, money today is worth more than the same amount of money received in the future.

PayFi’s goal is to help users and customers maximize the time value of money. For example, Buy Now Pay Never uses the time value of money for payments, while Creator Monetization and Account Receivable involve obtaining present money by paying the time value of money, similar to Buy Now Pay Later.

Overall, PayFi is not an entirely new concept. The issues it seeks to address already exist in the traditional financial system, and there are solutions in place. However, this does not mean that PayFi lacks value because traditional solutions are still not good enough.

Take corporate financing as an example. Accounts receivable are a form of corporate financing. In actual production, financial institutions face challenges in simplifying the evaluation and execution processes for collateral to meet policy and risk control requirements.

This complexity often makes it difficult for small and medium-sized enterprises (SMEs) to secure financing, leading to reluctance to pursue financing and failing to fully utilize the time value of money.

In the context of cross-border payments, the time value of money is even more evident. Cross-border payments rely heavily on correspondent banks, SWIFT, and other long-established financial networks, which cannot transfer funds between countries in real-time.

As more customers demand next-day or same-day settlement, financial institutions need to pre-fund accounts in various countries (similar to how Orbiter handles cross-chain transactions between different bridges). This is known as prefunding accounts.

According to a study by Arf, over $4 trillion was locked in prefunding accounts globally in 2022, representing a significant opportunity cost for financial institutions.

Therefore, PayFi still has immense potential value to be explored. Just as electric cars have revolutionized the automobile industry, even if PayFi seems like an old concept in a new package, the core issue is whether it can use blockchain technology to optimize the existing system and deliver user experiences that the old system and tech stack could not achieve, ultimately driving a revolution.

Notable Projects in the PayFi Space

Currently, there are not many projects focusing on the “PayFi” concept, as it remains in its very early stages. Below are some key PayFi-related projects to help readers better understand the developments within this emerging sector.

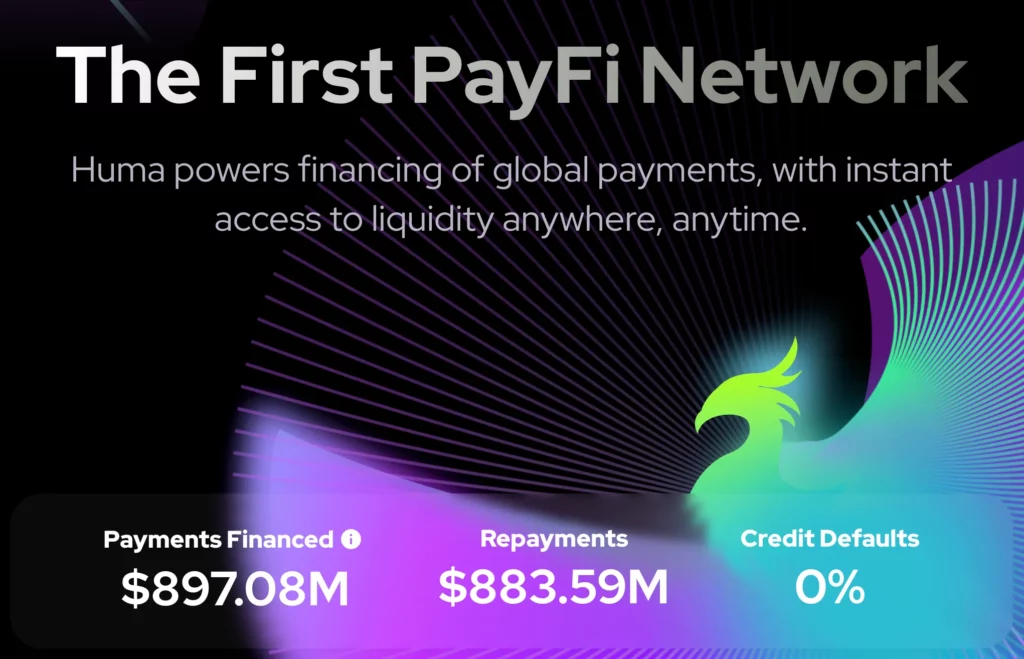

Huma

Huma is one of the most prominent protocols associated with the PayFi concept. As of August 16, 2024, the platform has facilitated nearly $897 million in payment financing with a default rate of 0%.

Huma currently operates two versions, V1 and V2. Huma V1 is a lending protocol for businesses and individuals, allowing users to borrow against future income (Real World Assets, or RWA) as collateral. Huma V2 builds on V1 by adding accounts receivable purchasing functionality.

On the Huma platform, there are various pools tailored to different purposes and partners. However, Huma is still somewhat distant from the decentralized, no-barrier, identity-independent financial products envisioned by the blockchain community.

When the author attempted to borrow or provide funds on Huma, they encountered several obstacles such as difficulty finding the entry point, KYC requirements, and other usage barriers, which could deter potential users.

Arf

Arf is a cross-border payment network project that provides unsecured, short-term, USDC-based working capital credit lines to licensed financial institutions. This allows these institutions to conduct cross-border payments smoothly without needing additional collateral or pre-funding accounts.

For example, if an Arf client in Europe wants to remit funds to a partner in Africa, the client only needs to transfer funds to Arf’s local bank account. Arf will then convert the USDC into the local fiat currency for same-day settlement. After the transaction is completed, the client can deposit funds into Arf’s account via Wire, SWIFT, etc., and Arf will immediately convert these deposits into USDC to ensure liquidity.

Arf completed a $13 million seed round in 2022. So far, Arf’s services are still focused on enterprises, and becoming a customer requires filling out an application form. In April of this year, Arf announced a merger with Huma. Currently, about 70% of the nearly $890 million in payment financing on the Huma platform comes from Arf. The combination of Arf’s liquidity and Huma’s platform could potentially create significant synergies.

Credix Finance

Credix is a B2B credit protocol within the Solana ecosystem, with a product logic very similar to Huma’s. The Credix platform offers investment pools tailored to specific types of investors. Institutional investors who have completed KYC can provide liquidity to these pools to offer credit. Credix’s services are currently concentrated in Latin America, focusing on areas like accounts receivable financing.

Compared to Huma, Credix has higher requirements for investors and supports a narrower range of businesses. As a result, Credix has issued fewer loans than Huma and Arf. Additionally, Credix has launched a feature called CrediPay, which offers “Buy Now Pay Later” services for businesses.

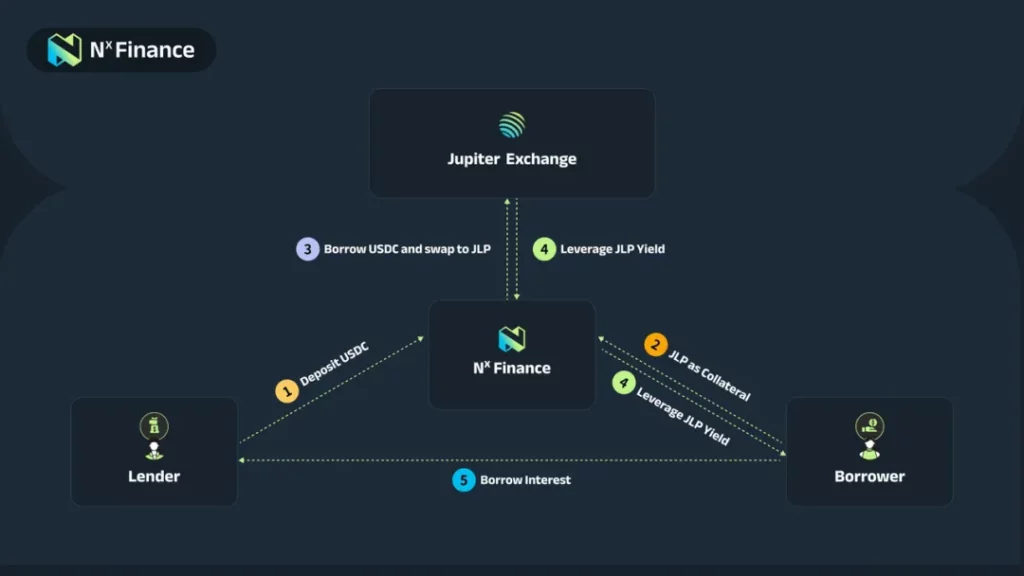

NX Finance

Lastly, there is NX Finance, a yield-layer protocol on Solana. NX Finance provides users with strategies for leveraging or farming interest-bearing assets within the Solana ecosystem. These two strategies are called the Fulcrum Strategy and the Gold Mining Strategy on NX Finance. Currently, NX Finance is still in its early stages, with a total value locked (TVL) of around $14 million.

Fulcrum Strategy: This strategy allows users to leverage premium interest-bearing assets (currently supporting JLP). Lenders deposit USDC to earn interest from borrowers, while borrowers must collateralize premium assets (JLP) to obtain loans. A portion of the loan is used to purchase JLP to increase the JLP holding, meaning the borrower receives leveraged returns in JLP rather than USDC.

Strictly speaking, NX Finance is different from the above projects and is not a PayFi project per se. It is more akin to a crypto-native lending protocol.

However, in a broader sense, lending protocols are a crucial component of fully utilizing the time value of money, which is essential for achieving concepts like Buy Now Pay Never.

Ultimately, whether a project qualifies as PayFi depends on whether the services it provides address real production and consumption needs rather than being purely financial leverage mechanisms.

Connecting and integrating these real-world demands require substantial effort from the project team, such as obtaining licenses.

Conclusion

Overall, PayFi is still in a very early stage, and many projects claiming to be PayFi have not yet launched. Currently, PayFi can be seen as a subset of the Real World Asset (RWA) sector, primarily focused on iterating around Web2 needs like accounts receivable financing and cross-border payments.

Additionally, the envisioned “openness” of PayFi is still far from being realized, as most existing projects impose strict KYC and geographic restrictions on users. Nevertheless, some PayFi projects, such as Huma, have already accumulated enough data to demonstrate a demand for their products.

As a sector that is currently distant from on-chain users and exchanges, it remains to be seen whether PayFi can create more innovative products centered around the time value of money and other attributes of currency.

It will also be interesting to see if PayFi can accommodate more physical asset classes and improve the liquidity of these assets. These are questions worth long-term attention from investors.

-

-

-

-

-

-

-

-