How to Determine Cost Basis for Cryptocurrency Tax Reporting?

Determining the cost basis for cryptocurrency for tax purposes involves considering the purchase price, transaction fees, and events such as hard forks or staking rewards.

1. What is the Cost Basis of Cryptocurrency?

In the context of cryptocurrency, “cost basis” refers to the initial expenditure paid for the digital asset. This is an important consideration when calculating capital gains or losses upon the sale or disposal of cryptocurrency. The capital gain or loss from selling cryptocurrency is calculated as the selling price minus the cost basis.

Accurately reporting the cost basis is crucial to avoid tax complications, which could result in underpayment or overpayment of taxes and potential penalties from tax authorities. Given the increasing scrutiny from tax authorities worldwide on cryptocurrency transactions, accurate reporting has become more important.

In many jurisdictions, including the United States, tax authorities require individuals to report cryptocurrency transactions for tax purposes. Inaccurate reporting of the cost basis can lead to fines and audits. Therefore, investors must keep comprehensive records of all cryptocurrency transactions, including purchase prices, transaction dates, and any additional fees.

2. Common Methods for Calculating Cryptocurrency Cost Basis

There are several methods to calculate the cost basis for cryptocurrency, as outlined below:

2.1 Specific Identification

The specific identification method is a common way to calculate the cost basis of cryptocurrency holdings. Investors can use this method to individually determine and track the cost basis of each cryptocurrency asset. When selling or disposing of a crypto asset, investors identify the exact units being sold and their purchase price.

This method allows for accurate calculation of the cost basis as it considers the specific purchase price of the sold units. This is particularly useful for investors looking to optimize tax outcomes by carefully choosing which units to sell based on their cost basis and holding period.

For understanding how this method works, consider a hypothetical example: An investor buys 1 Bitcoin for $30,000 on January 1, 2023, and another Bitcoin for $50,000 on May 1, 2023. If the investor decides to sell 1 Bitcoin, they can choose which specific purchase to use as their cost basis.

Implementing the specific identification method requires meticulous record-keeping of each cryptocurrency transaction, including purchase prices, dates, and any related fees. Despite its potential for the highest accuracy in cost basis reporting, it may be more challenging and time-consuming to execute compared to other methods.

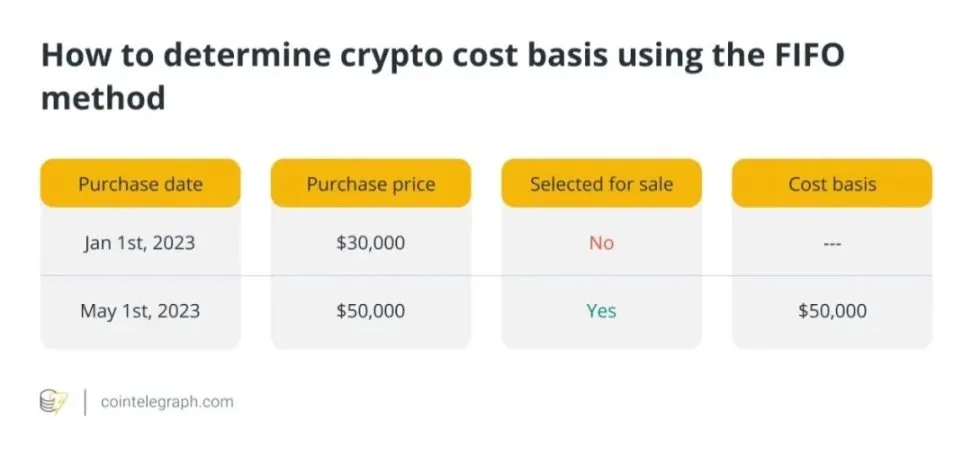

2.2 First-In, First-Out (FIFO)

Another common method for calculating the cost basis of held cryptocurrency is the “First-In, First-Out” (FIFO) method. Under FIFO, the earliest purchased cryptocurrency assets are assumed to be the first sold. This method presumes that the longest-held cryptocurrency is being sold or otherwise disposed of, making it easier to track transactions.

Suppose an investor buys 1 Bitcoin for $30,000 on January 1, 2023, and another Bitcoin for $50,000 on May 1, 2023. When they sell 1 Bitcoin, the earliest purchase price (i.e., $30,000) is automatically used as the cost basis.

Although simple to implement, FIFO might lead to higher tax costs in certain cases, as it can result in selling assets with lower purchase prices first, thereby increasing capital gains.

Despite this drawback, FIFO remains a popular choice among many investors due to its simplicity, making it preferred by those who do not actively trade cryptocurrencies and who wish to simplify their tax calculations.

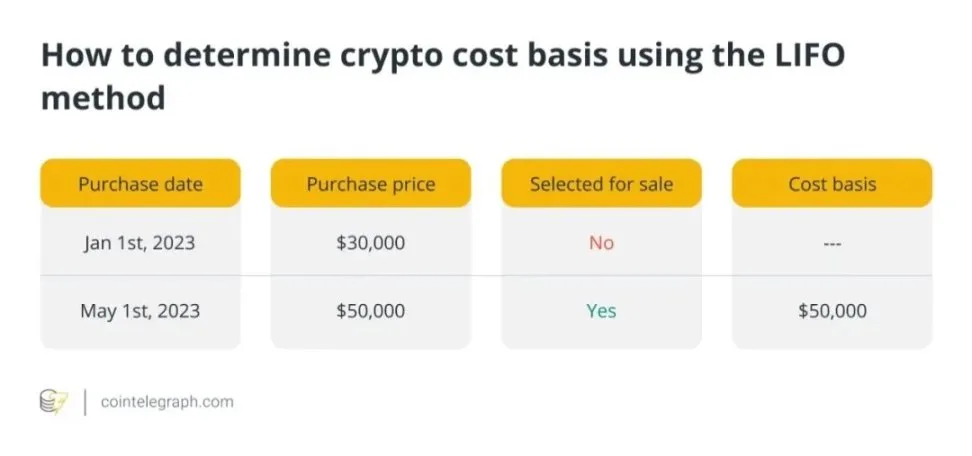

2.3 Last-In, First-Out (LIFO)

Contrary to First-In, First-Out (FIFO), “Last-In, First-Out” (LIFO) assumes that the most recently purchased cryptocurrency assets are sold first, using the latest purchase price as the cost basis.

Suppose an investor buys 1 Bitcoin for $30,000 on January 1, 2023, and another Bitcoin for $50,000 on May 1, 2023. When they sell 1 Bitcoin, the most recent purchase price is automatically used as the cost basis.

LIFO might be beneficial in certain situations, particularly when prices are rising. By selling the most recently acquired assets first, investors can minimize capital gains and, consequently, reduce tax liabilities. However, if the most recently acquired assets have a lower cost basis than older assets, LIFO could result in higher taxes.

While LIFO may offer tax benefits compared to FIFO, it is less commonly used to determine cryptocurrency tax liabilities. This is because LIFO can be more complex and may require more thorough record-keeping.

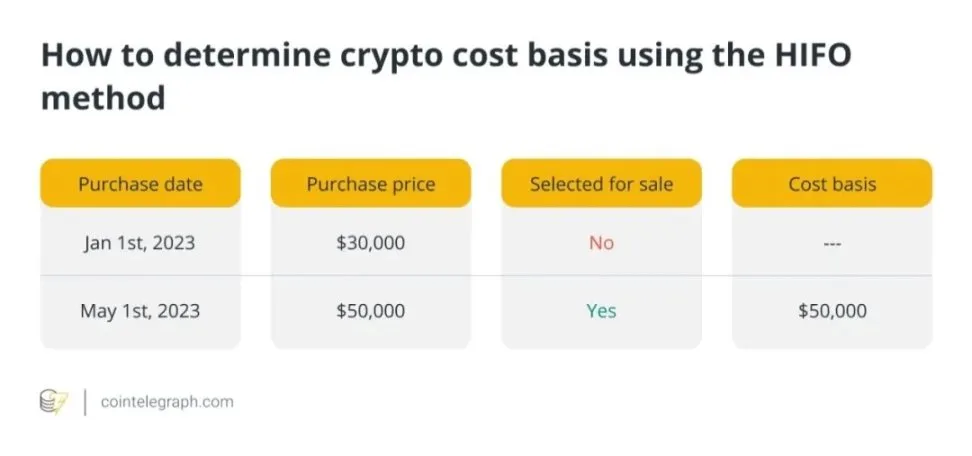

2.4 Highest-In, First-Out (HIFO)

The “Highest-In, First-Out” (HIFO) method is a strategic approach to determining the cost basis for cryptocurrency holdings for tax purposes. It assumes that the most expensive cryptocurrency assets are sold first, contrary to FIFO and LIFO.

By selling the assets with the highest cost basis first, investors can strategically reduce capital gains and, therefore, lower their tax liabilities. This strategy is particularly advantageous when prices have risen, and the sold assets have a high cost basis.

To understand how HIFO works, consider this example: An investor buys 1 Bitcoin for $30,000 on January 1, 2023, and another Bitcoin for $50,000 on May 1, 2023. When they sell 1 Bitcoin, the highest purchase price is automatically used as the cost basis.

While HIFO can minimize capital gains taxes, it may not be suitable for all investors due to the need for detailed records. Moreover, investors must ensure they retain appropriate documentation to support their calculations, as tax authorities might scrutinize the use of HIFO. Despite these challenges, HIFO can be adopted by investors seeking to reduce their cryptocurrency tax liabilities.

2.5 Average Cost Basis (ACB)

By using this technique, investors can calculate the average price of all their held cryptocurrency. This average price is then used to determine the cost basis of the sold crypto assets.

Assume an investor buys 2 Bitcoins, one for $30,000 (on January 1, 2023) and another for $50,000 (on May 1, 2023). Their average cost basis calculation would be as follows:

The average cost method offers a middle ground between potential tax optimization and simplicity. Using the average price for all holdings of the same cryptocurrency can simplify cost basis calculations. Investors who frequently buy and sell cryptocurrencies and wish to streamline their record-keeping process may find this strategy helpful.

While the average cost method may not offer the same tax efficiency as methods like FIFO or HIFO, it remains a popular choice for investors. It still provides reasonable accuracy in cost basis reporting and helps ensure compliance with tax requirements.

3. Documentation Needed for Accurate Cost Basis Calculation

For cryptocurrency, complete transaction records are essential for accurate cost basis assessment. Investors need to maintain detailed records of the following data:

- Purchase Date and Time: The date and time when the cryptocurrency was purchased.

- Purchase Price: The cost incurred to acquire the cryptocurrency.

- Transaction Fees: Any fees paid during the purchase (e.g., gas fees).

- Transaction Type: Whether it was a purchase, sale, exchange, or another type of transaction.

- Wallet Address: Addresses involved in the transaction.

- Transaction ID: Unique identifier assigned to each transaction.

Record-keeping is crucial for tax reporting to ensure compliance with tax laws and reduce the possibility of errors or discrepancies in capital gains calculations. Additionally, thorough record-keeping can help investors adequately respond to any audits or inquiries from tax authorities.

4. Differences in Cryptocurrency Cost Basis Calculation Across Jurisdictions

Different countries employ various methods to determine the cost basis of cryptocurrency, affecting investors’ tax liabilities. The “Pooling” strategy, a modified form of the average cost basis method, is the most widely used technique in the United Kingdom. Investors using this strategy calculate the average cost of all identical cryptocurrencies held to determine the taxable cost basis.

Canada typically employs the specific identification method to facilitate tax optimization. The United States allows specific identification but tends to use the FIFO method as the default.

Australia uses several methods, such as specific identification, FIFO, and, in some cases, the average cost basis method. It’s essential to remember that some tax regulations may change, so seeking professional advice specific to your jurisdiction is always the safest approach.

5. Calculating Cost Basis for Different Types of Cryptocurrency Transactions

Calculating the cost basis for different types of cryptocurrency transactions requires special considerations:

5.1 Purchasing Cryptocurrency

The amount paid to purchase cryptocurrency constitutes its cost basis. This includes the price of the cryptocurrency and any transaction fees paid at the time of purchase.

Example: If an investor pays $10,000 to purchase 1 Bitcoin and incurs a $20 transaction fee, the total cost basis is $10,020.

5.2 Selling Cryptocurrency

The capital gain or loss from selling cryptocurrency is calculated by subtracting the cost basis from the selling price. The initial purchase price of the cryptocurrency, plus any transaction fees paid at the time of purchase, constitutes the cost basis.

Example: If an investor sells 0.5 Bitcoin for $7,000, with a cost basis of $6,020 (plus a $20 transaction fee), the capital gain is $980.

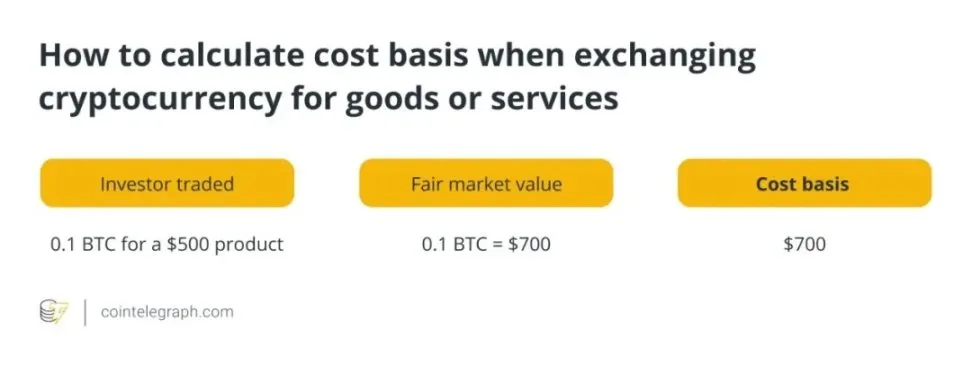

5.3 Exchanging Cryptocurrency for Goods or Services

The fair market value of the cryptocurrency at the time of the transaction is the cost basis for exchanging it for goods or services. It is determined by the dollar value of the cryptocurrency at the time of the transaction.

Example: If an investor exchanges 0.1 Bitcoin for a product valued at $500, and the fair market value of 0.1 Bitcoin at the time of the transaction is $700, the cost basis of the transaction is $700.

5.4 Receiving Cryptocurrency as Income or Gifts

The fair market value of the cryptocurrency at the time of receipt is the cost basis when receiving cryptocurrency as a gift or income. Typically, this amount is determined by the dollar value of

the cryptocurrency at the time of receipt.

Example: If an investor receives 0.2 Bitcoin as a gift with a fair market value of $1,300, then $1,300 will be the cost basis for the gifted Bitcoin.

6. Handling Various Cryptocurrency Events for Cost Basis Calculation

6.1 Hard Forks and Airdrops

The cost basis of new cryptocurrency received through hard forks and airdrops is generally considered to be $0. However, it is crucial to track the fair market value of the cryptocurrency at the time of receipt as it will be used to determine the capital gain or loss when the new cryptocurrency is sold or otherwise disposed of.

Example: If a hard fork or airdrop results in an investor receiving 5 units of new cryptocurrency, each with a fair market value of $100 at the time of receipt, then $500 will be the cost basis for the new cryptocurrency.

6.2 Staking and Mining Rewards

Rewards from staking and mining are usually recognized as income at the fair market value of the cryptocurrency on the day they are received. The fair market value becomes the cost basis of the received cryptocurrency.

Example: If an investor receives 5 units of cryptocurrency as staking rewards, and each unit has a fair market value of $40 at the time of receipt, the cost basis for the staking cryptocurrency is $200.

6.3 Exchanging One Cryptocurrency for Another

The fair market value of the cryptocurrency given up at the time of the exchange is used to determine the cost basis of the new cryptocurrency received through the exchange. This fair market value becomes the cost basis for the new cryptocurrency.

Example: If an investor exchanges 2 Bitcoins for 100 units of another cryptocurrency, and the fair market value of the 2 Bitcoins at the time of the exchange is $150,000, then the cost basis for the new cryptocurrency is $150,000.

7. Adjusting Cryptocurrency Cost Basis for Transaction Fees and Other Expenses

The cost basis of cryptocurrency assets must be adjusted for transaction fees and other related expenses. One way to achieve this is to include transaction costs in the cost basis. For example, when purchasing cryptocurrency, the total cost basis should include any fees paid during the transaction in addition to the purchase price of the asset. Similarly, any transaction fees related to selling cryptocurrency should be deducted from the proceeds.

Besides transaction fees, investors should also consider exchange fees and other expenses. Including these costs (the fees charged by cryptocurrency exchanges to execute transactions) in the total cost basis calculation is crucial. By considering transaction fees and other related expenses, investors can ensure that their cost basis calculation accurately reflects the total investment in purchasing and disposing of crypto assets.

8. Benefits of Using Crypto Tax Software for Accurate Tax Reporting

Using crypto tax software for tax reporting offers numerous advantages. Firstly, it saves investors time and reduces the likelihood of errors in tax filings by automatically calculating capital gains and losses. These platforms can easily integrate with wallets and cryptocurrency exchanges, automatically importing transaction data and generating comprehensive reports for tax purposes.

Secondly, crypto tax software ensures compliance with tax requirements by using appropriate cost basis techniques and considering transaction fees and other expenses. Investors can reduce the risk of audits or fines from tax authorities by adequately disclosing their cryptocurrency transactions.

These platforms also provide real-time tax estimates, allowing investors to assess their annual tax liabilities and make informed decisions about their cryptocurrency holdings. Moreover, many crypto tax software solutions offer tax-loss harvesting features, enabling investors to strategically sell assets to offset gains, thereby optimizing their tax outcomes.