Exploring Solana’s Fee Market and the New Future of MEV

As DeFi expands rapidly, the Solana blockchain is emerging as a new hotspot for decentralized applications, thanks to its high-performance architecture and innovative technology. However, as economic activity surges, concerns about Solana’s fee market and Maximum Extractable Value (MEV) are gradually becoming the focus of community attention.

The Rise of Solana in DeFi

The rise of Solana is expanding the DeFi space. While we’ve been observing from afar, we’ve never offered a new perspective. However, the fervent activity on Solana in recent months has provided us with a new opportunity to observe its position in the market and how it may evolve.

Transaction fees are essential for supporting the most basic activities on a blockchain, as they validate users’ transactions and include them in a block. The primary purpose of these fees is to prevent spam; they are also part of the subsidy paid to validators for building/validating blocks. In a sense, these network fees are similar to rent; users pay fees to access a limited commodity per unit of time. The commodity here is “block space,” i.e., space on the block.

Here, we evaluate the block space on two of the largest smart contract blockchains, Ethereum and Solana. As we delve deeper, we understand that the fee market, both designed within the protocol and organically developed from the ground up, allows validators to leverage their access to block space.

Solana’s fee market is optimized for high performance and aims to avoid the problems seen in Ethereum’s approach. However, while Solana’s market may ultimately be more efficient than Ethereum’s, it still needs to undergo a similar MEV revolution (validators starting to exploit their privileged position). Solana doesn’t need to go the route of Ethereum’s proposed Protocol Blockchain Separation (PBS), but it needs to identify a comprehensive approach to long-term stability of its fee market.

Fundamentals of Block Space Valuation

Before we delve deeper, let’s try to understand how the value of block space is roughly determined.

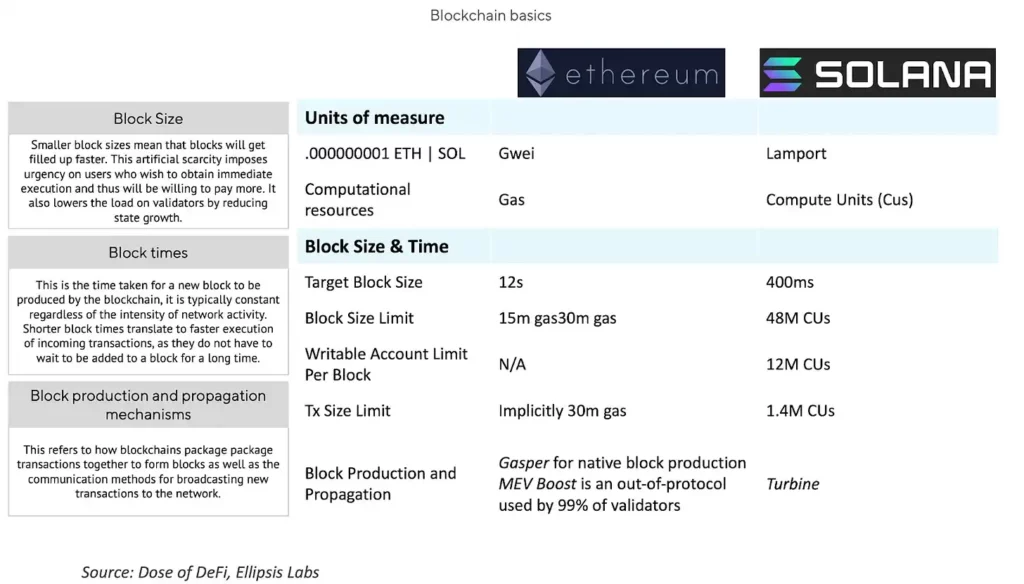

There are both technical aspects and social aspects (essentially the coordination among various parties that give value to the blockchain). Technically, blockchains can adjust block size, block time, and block production and propagation mechanisms. The chart below provides a more detailed description and comparison of Ethereum’s and Solana’s approaches.

The social aspect refers to the coordination among stakeholders to achieve the technical and financial goals of the chain. It can also be seen as the social status of the blockchain, subjective but an important metric nonetheless. Just as effective as social pressure and building a culture to solve problems, both Solana and Ethereum have built such cultures. Recent examples of discussions around the social layer include debates on increasing Ethereum’s gas limit and the issuance per epoch, as well as the recent closure of Jito’s mempool on Solana.

Now, let’s examine and compare the fee markets of Ethereum and Solana in more detail.

Summary of Ethereum’s Fee Market

Ethereum’s popularity is primarily attributed to its execution environment: the Ethereum Virtual Machine (EVM), which makes smart contracts possible. Another factor is Ethereum’s permissionless nature, which has led to various waves of innovation: the ICO boom of 2017-2018, DeFi Summer of 2020, and the NFT craze of 2021-2022. The continued existence of these applications has created value for validators who provide block space for these activities.

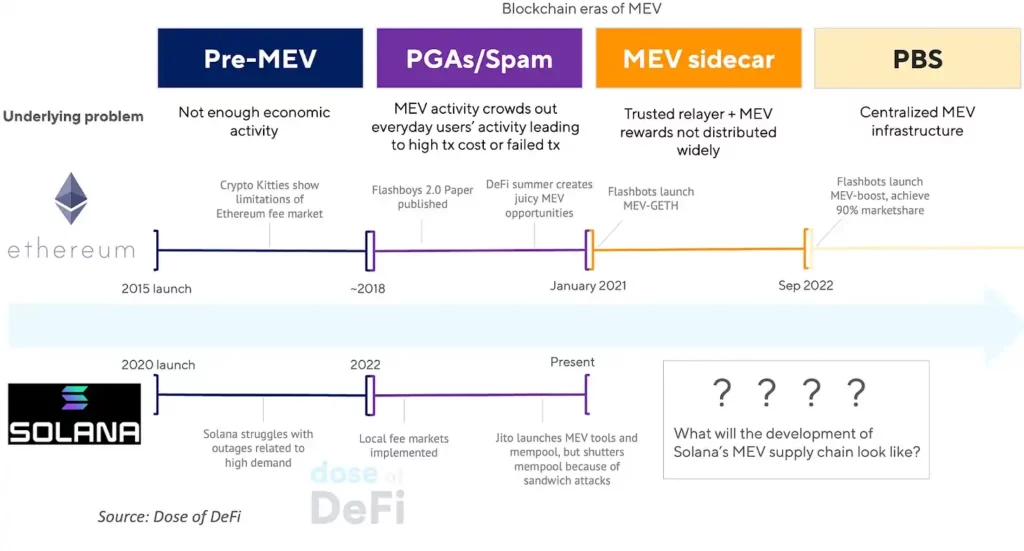

Shortly after a surge in economic activity on Ethereum (this was before the transition to PoS), miners began exploring how to insert their transactions when arbitrage opportunities arose, leveraging their position as block proposers.

Phil Daian was the first to document this activity. He first documented this activity in his groundbreaking paper, Flash Boys 2.0, published in 2019 (which we now call MEV). At the time, Ethereum’s fee market only allowed higher gas prices as an incentive for transaction inclusion. These Priority Gas Auctions (PGAs) congested the Ethereum network and drove up gas prices until Flashbots (co-founded by Daian) was launched. This created a market for miners who could be paid transaction inclusion fees by searchers, who are on-chain arbitrage traders. Ethereum researchers subsequently realized that MEV extraction could be more powerful than on-chain fees.

The most significant change to Ethereum’s fee market may be EIP-1559, which created a base fee (dynamically determined per period, to prevent spam, and burned), and a priority fee (used to display urgency or specify preferences and paid to block proposers for transaction inclusion). An important point is that the “priority fee” is functionally different from “tips.” The former ensures inclusion and is mediated by the underlying chain, while the latter ensures ordering and inclusion and is mediated by the fee market.

Ethereum’s approach has been evolving; check out our in-depth study of MEV from last autumn. This has happened through a combination of the social layer, which attempts to decentralize a concentrated MEV industry, and the technical layer, where MEV has now become a key part of the technical roadmap (Vitalik calls this part of the roadmap “The Scourge”).

Mechanics of Solana’s Fee Market

Solana takes a radically different approach in blockchain architecture, especially in scalability.

Some notable innovations of Solana include:

- No General Memory Pool: In Solana, transactions are forwarded directly from the initiating client to the current Leader responsible for block generation, eliminating the need for a memory pool. This theoretically reduces transaction confirmation latency, but in practice, the situation is not always straightforward due to “jitter” (i.e., different processing times experienced by different validators when handling transactions or blocks).

- State Isolation: Lack of a memory pool extension makes transactions on its dAPPs more independent of each other. This approach is similar to the concept of “adding more lanes to ease traffic”; different types of transactions on Solana must follow specific “paths,” from users to Leaders, to be added to blocks.

- Parallel Execution: Solana can process non-overlapping transactions simultaneously in the same block. This is due to two factors:

- Solana’s block production is (roughly) continuous, as Leaders are expected to add transactions to blocks as they receive them.

- Slot Leaders are fixed, as they are pre-scheduled in a queue and are also responsible for continuous production of four consecutive blocks.

These two factors, combined with Solana’s state isolation, enable transactions to be “multithreaded.” This means that transactions across multiple threads are roughly confirmed at the same time in the current epoch’s Leader schedule (provided transactions within the same thread do not change the same state) in the same way and at the same time.

Solana’s Fee Market: Cheaper ≠ Better

Network fees on Solana are typically very low (though they have risen with recent demand). In contrast to Ethereum, Solana has a static base fee measured in lamports. Then, its priority fee is measured in micro lamports per computational unit requested.

This means that while fees scale algorithmically with complexity and demand on the EVM, the SVM only needs to increase its priority charge through simple requests. The resulting non-dynamic technical issues are detailed here, but the main point is that pricing demand fluctuations statically for a commodity with determined supply is not ideal.

Solana’s Fee Market: Inevitability of MEV

Solana’s social consensus sees its low fees as a unique advantage compared to other blockchains. This approach invites spam, so some advocate for raising fees or implementing dynamic base fees during periods of high activity (similar to EIP-1559).

Solana’s approach so far has been to implement localized fee markets to handle increased demand. Since the state is isolated, the network can easily identify “hotspots” or states experiencing increased demand. This hotspot approach allows the blockchain to algorithmically price transactions with higher target transaction fees than less in-demand states. This approach is similar to Ethereum’s block builder role completed by a scheduler, which helps place transactions into consecutive blocks based on priority fees.

As part of implementing localized fee markets, Solana has built an in-protocol scheduler that locally schedules transactions to execute based on a first-in, first-out algorithm. Transactions are continually streamed to slot Leaders, who then sort them based on the hints they provide.

The algorithm also requires slot Leaders to share the shards they are building with some of the nodes they are connected to, based on their stake. However, as mentioned earlier, this process is disrupted by jitter. Specifically, scheduler jitter (due to Solana randomly assigning incoming transactions to execution threads) and network jitter (from P2P relay latency of incoming transactions and shards) create uncertainty in transaction ordering on Solana, making block space auctions economically feasible. In other words, validators have an economic incentive to insert or reorder transactions whenever there is jitter. For users, this means MEV leakage, and for validators, it means MEV profits.

Solana vs. Ethereum

A quick review of MEV on Ethereum: Before Flashbots on Ethereum, MEV activity crowded out regular blockchain activity, driving up gas prices for all users through PGAs. On Solana, fees don’t skyrocket because it lacks shared state and a global minimum price like Ethereum, but during increased activity, regular users find it challenging to complete transactions on Solana. Flashbots released MEV-GETH to handle PGAs, creating a separate channel for MEV value capture outside the in-protocol fee mechanism. In the case of Solana, Jito introduced a similar product for validators, providing them with a pseudo memory pool and a custom scheduler to order transactions most advantageously. Jito’s memory pool was attractive to users, offering them a guarantee of inclusion (i.e., their MEV being extracted).

While a popular product, Jito’s memory pool came under social pressure and was shut down last month. This may be for the same reasons that over 20% of Ethereum transactions run through private memory pools: users grow weary of sandwich attacks. Spam is once again the only mechanism for time-sensitive transactions on Solana (from a probabilistic standpoint). The lack of an efficient block space bidding mechanism leads to uncertainty during periods of high demand.

Since transactions on Solana now stream directly to slot Leaders and the priority model has been disrupted, the topology (and resulting latency) is a crucial component of users considering time-sensitive transactions.

The topology of users in the network can be understood as how “far” they are from Leaders, depending on their stake weight and/or the stake weight of nodes they are connected to. Thus, rational agents will seek to be connected to nodes with high stakes already controlled, leading to centralization.

As a short-term consequence of spam, Solana is now so congested that it’s nearly unusable for less sophisticated users due to transaction failures. Therefore, addressing long-term consequences (centralization of co-location and network stakes) becomes more critical.

A More Rational Market Structure?

Solana’s initial design philosophy centered on eliminating user friction and allowing the validation network to meet demand in any way. What they overlooked is that markets operate most effectively when there is a certain degree of certainty in their operation. Fee markets provide a way to democratize inclusion by requiring users to pay more, shifting the problem from a topological perspective to an incentive-based one.

While this changes the user experience, accepting fee markets, especially their relationship with MEV, is the best way forward for Solana and its users. Providing a cost-intensive packet approach while maintaining the integrity of the chain is much better than having no method at all.

In fact, on-chain activity is almost always time-sensitive, especially when agents seek to extract value with little or no economic cost. High certainty execution is better than cheap probabilistic execution.

The specialization of fee markets allows bargaining and auctions for block space to occur at a higher level, away from consensus and execution. Thus, validators can fulfill their duties without worrying about optimizing the best outcome for accumulated block space value.

Solana’s Upcoming MEV Revolution

Solana is currently in discussions across the chain about how its fee market should be restructured (something Ethereum has been contemplating for years but hasn’t resolved).

Solana has not yet undergone the necessary MEV transformation. While the recent surge in on-chain activity has attracted MEV participants like Jito and Ellipsis to start building MEV infrastructure, major validators have not yet crossed this threshold to run their own Solana MEV strategies. In sharp contrast, all major stakers on Ethereum are running MEV. Solana’s validator community is not as adversarial as the Ethereum community, so for the sake of prioritizing end-user experience, both sides have reached a handshake agreement not to extract MEV (so far).

This situation won’t last; the social layer cannot monitor behavior indefinitely. Blockchains must operate in an environment of self-interested actors. Solana may perform better than Ethereum because it can address some MEV issues without being as severely constrained by decentralization. However, it still must answer some tricky questions, such as whether all staked SOL should be eligible for MEV rewards as achieved through MEV boost on Ethereum.

To address congestion issues on Solana, we’ve been exploring some minimal mechanisms. These mechanisms include dynamic fee structures, modifications to the upcoming local scheduler specification, stake-based constraints, and other optimizations at the application layer. Progress is happening quickly. The CEO of Jito recently admitted, “A small group of operators/searchers are sandwiching private mempools.”

MEV is a sign of economic growth, and therefore, it’s inevitable. In fact, even Bitcoin, whose simplicity is often hailed as its greatest feature, has begun to undergo a reshaping after Ordinals and the rise of economic activity. Choosing to ignore solutions because of negative externalities (such as Jito’s case) does not eliminate said externalities; it only leads to an uncoordinated market.

The social layer is an effective tool for preventing predatory behavior but can only last a short time. Ethereum is experiencing shortcomings at the social layer, with the rise of time games, a strategy where block proposers intentionally delay releasing their blocks for as long as possible to maximize MEV capture. This undermines the security of the chain but makes economic sense from the validators’ perspective. Shame can last for a while, but protocol research is the only long-term solution.

It’s too early to say what Solana’s MEV supply chain will look like in a few years. But one thing we can be sure of now is that most of the value will be captured by a large number of validators.