Over the past decade, cryptocurrency has transformed from a niche tech experiment into a mainstream financial tool. Web3 payment systems, powered by blockchain technology, offer transparency, security, and immutability in transactions. These systems are increasingly integrated into e-commerce platforms, point-of-sale systems, and peer-to-peer payment applications, making cryptocurrency more accessible in everyday life.

By 2023, the Web3 payments market had reached a valuation of $1.2 billion, and it’s expected to grow at a compound annual growth rate (CAGR) of over 15% from 2024 to 2032. Web3 payments are predicted to become a significant pillar of the digital economy, bringing new opportunities and challenges to the global financial ecosystem, much like traditional payment systems.

The Current Web3 Payment Infrastructure

Today’s Web3 payment infrastructure has simplified traditional payment processes by reducing the number of parties involved. Typically, a transaction only requires three participants: the payer, the receiver, and the blockchain (as the intermediary).

Since the blockchain is not a conscious entity, one could argue that only two active participants are involved, offering advantages in both speed and cost. All Web3 payment protocols rely on the same basic infrastructure, though specific implementations may vary slightly.

Protocols like Sphere Pay and Loopcrypto.xyz are notable for enabling businesses to integrate Web3 payment functionalities seamlessly, offering unique features that will be discussed further below.

What is PayFi?

As decentralized finance (DeFi) merges with payment systems, a new model called PayFi has emerged. PayFi creates a financial marketplace centered around the time value of money. It offers a way to leverage future funds for present needs—something traditional finance cannot provide.

PayFi consists of multiple payment forms, such as:

- Payment Tokens representing tokenized U.S. Treasury yields or yield-generating stablecoins.

- DeFi Lending to finance real-world assets (RWAs), generating on-chain returns for real-world payment scenarios.

- Next-generation Web3 Payment Systems that seamlessly integrate with DeFi protocols.

- Blockchain-based Traditional Payment Logic, aimed at constructing a comprehensive Web3 payment framework.

A prime example of PayFi in action is Ondo Finance, a protocol that tokenizes U.S. Treasuries to give more people access to institutional-grade financial products. Ondo Finance brings low-risk, stable returns, and scalable financial products—such as U.S. Treasuries and money market funds—onto the blockchain, allowing stablecoin holders to earn yields on their assets.

Ondo Finance offers two key products: OUSG and USDY. OUSG is a tokenized U.S. Treasury fund, while USDY is a yield-generating stablecoin backed by short-term U.S. Treasuries. As of August 2024, these products had a total value locked (TVL) of $556 million.

Through USDY, holders can not only have their assets valued in dollars but also earn yield, adding practical utility to payment tokens and accelerating the growth of PayFi in Web3.

Fascinating Innovations in Web3 Payments

Below are some intriguing and lesser-known innovations in the Web3 payments space, excluding crypto cards and on/off ramps.

Karrier One (Payments x DePIN)

The integration of payments with DePIN (Decentralized Physical Infrastructure Networks) has a practical application in telecom networks.

Karrier One is a carrier-grade decentralized network that incorporates payment and DePIN features. It operates through three modules: telecom infrastructure, blockchain technology, and the Karrier Numbering System (KNS).

Collaborating with global telecom providers, Karrier One offers seamless global communication coverage, and its governance is managed by the Karrier DAO, allowing token holders to participate in decision-making.

Through KNS, users can link their Web3 wallets directly to their phone numbers, enabling them to participate in DeFi activities and facilitate smooth payment flows. With 7.1 billion mobile phone users globally, Web3 telecom networks present massive growth potential.

Huma Finance

Huma Finance is a lending protocol that facilitates income-based borrowing. It connects borrowers to global on-chain investors, allowing them to secure loans against future earnings.

The protocol includes standard credit facilities and decentralized signaling and evaluation agents, which assess income sources, evaluate credit, and manage ongoing risk.

As of August 2024, Huma had raised nearly $900 million in loans, with $883 million successfully repaid and a 0% default rate.

Sphere Pay

Sphere offers an API specifically designed for digital currency payments, providing users with a seamless experience that connects them to stablecoins, thereby accelerating Web3 payment adoption.

Sphere offers merchants customizable or ready-made front-end solutions for easy integration, along with various pricing models to meet different product or service needs.

Sphere charges no software fees, taking a fixed 0.3% fee per transaction, making it ideal for small businesses with low transaction volumes or startups with low initial costs.

Loopcrypto.xyz

Loop is a Web3 payment infrastructure that helps companies streamline or automate collections and payments. Through automated payment features, Loop improves operational efficiency and reduces customer churn.

The platform supports all ERC-20 tokens and provides settlement in either cryptocurrency or fiat, simplifying corporate financial operations.

Loop is easy to integrate, reducing the barriers for businesses adopting crypto. It also works with top platforms like Stripe, Zapier, and Xero, allowing businesses to incorporate crypto payments into their existing financial management systems without significant system overhauls.

Orbita

Orbita is a decentralized Layer 1 payment protocol being developed on the Cosmos ecosystem. Although it has yet to launch its testnet, the team is likely still writing documentation and a whitepaper.

Orbita’s key features are expected to include direct irreversible payments, reversible payments, decentralized subscriptions, and e-commerce integration.

As a payment-focused Layer 1 protocol, it represents a new frontier in the payment industry and could bring exciting developments to the space.

Market Data & Updates

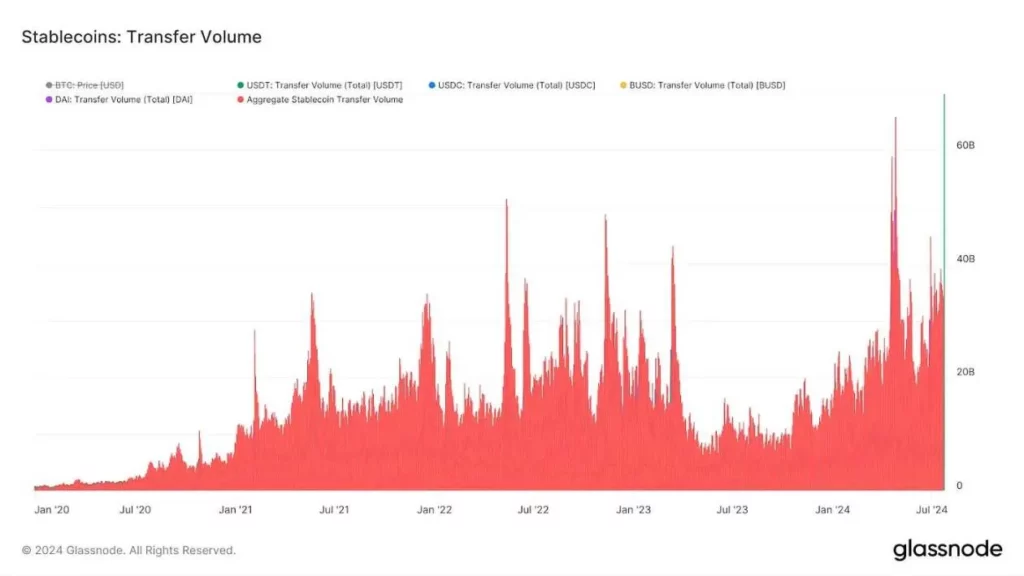

The rise of cryptocurrency over the last decade has driven the rapid growth of stablecoins. Their total market cap surged from $20 million in 2017 to $170 billion in 2024. At its peak in 2024, stablecoin transfer volumes hit $60 billion. As this trend continues, the demand for payment systems that accommodate stablecoins will only increase.

Key stablecoin providers are also expanding their market presence. For example, Tether recently announced plans to launch a dirham-backed stablecoin in the UAE, aiming to become the leading digital payment token in the region. Circle’s CEO, Jeremy Allaire, revealed plans for an iPhone tap-to-pay feature for USDC, following Apple’s decision to allow third-party developers access to the iPhone’s secure payment chip.

Paypal has been actively promoting PYUSD since entering the stablecoin market in August 2023. By mid-2024, PYUSD had become the sixth-largest stablecoin, surpassing established tokens like FRAX and BUSD.

Reflections: The Impact of Web3 Payments

Web3’s strength lies in its ability to facilitate secure, low-cost, and near-instantaneous global transactions. While still in its early stages, institutions, businesses, and individuals are already adopting blockchain for payments.

If Web3 payments become mainstream, how will banks respond to reduced intermediary fees? Some banks are already developing private blockchains, but their revenue will likely still be lower than today’s fees. While there will likely be resistance, adoption at the retail level may take time, especially since private blockchains retain the traditional opacity and centralization of banks.

Although Web3 payments excel in global trade, the impact on local needs remains minimal. For everyday transactions, such as paying at a grocery store, there may be little incentive to switch from a traditional bank card to cryptocurrency.

I believe that with proper regulatory catalysts, Web3 payments could thrive. Even without clear regulatory frameworks, as seen in recent years, the market may continue to grow. Ultimately, I remain optimistic that Web3 payments will become a standard option, no longer questioned but embraced as a natural choice.

-

-

-

-

-

-

-

-