Stablecoins are among the most transformative payment forms since credit cards, reshaping how money flows. With low cross-border transfer fees, near-instant settlements, and access to widely demanded global currencies, stablecoins have the potential to iterate on today’s financial system. For institutions holding dollar deposits that support digital assets, the stablecoin business also presents significant profit opportunities.

Currently, the global supply of stablecoins exceeds $150 billion, with five stablecoins—USDT, USDC, DAI, First Digital USD, and PYUSD—each boasting a circulation of at least $1 billion. I believe we are heading toward a future where every financial institution issues its own stablecoin.

Reflecting on this growth, I conclude that examining the evolution of other payment systems, particularly credit card networks, could provide valuable insights.

Similarities Between Credit Card Networks and Stablecoins

For consumers and merchants, stablecoins should function like dollars. However, each stablecoin issuer treats the dollar differently due to variations in issuance and redemption processes, reserves backing each stablecoin, regulatory environments, and the frequency of financial audits. Addressing this complexity presents a substantial opportunity.

We’ve seen similar situations in the credit card industry. Consumers use assets that are nearly equivalent to dollars but not fully interchangeable—these are dollar-denominated loans tied to individual credit scores. Networks like Visa and Mastercard coordinate the payment process, and the stakeholders (or potential stakeholders) in both systems are quite similar: consumers, their banks, merchants’ banks, and the merchants themselves.

To illustrate this network structure, consider a simple example:

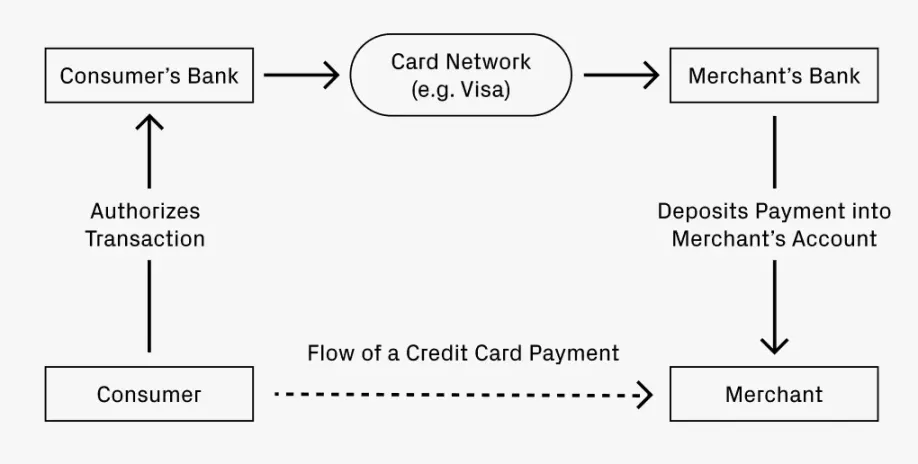

Imagine dining at a restaurant and paying with a credit card. How does your payment reach the restaurant’s account?

- Your bank (the credit card issuer) authorizes the transaction and sends funds to the restaurant’s bank (the acquiring bank).

- A clearing network, such as Visa or Mastercard, facilitates the fund transfer, charging a small fee.

- The acquiring bank deposits the funds into the restaurant’s account, deducting a service fee.

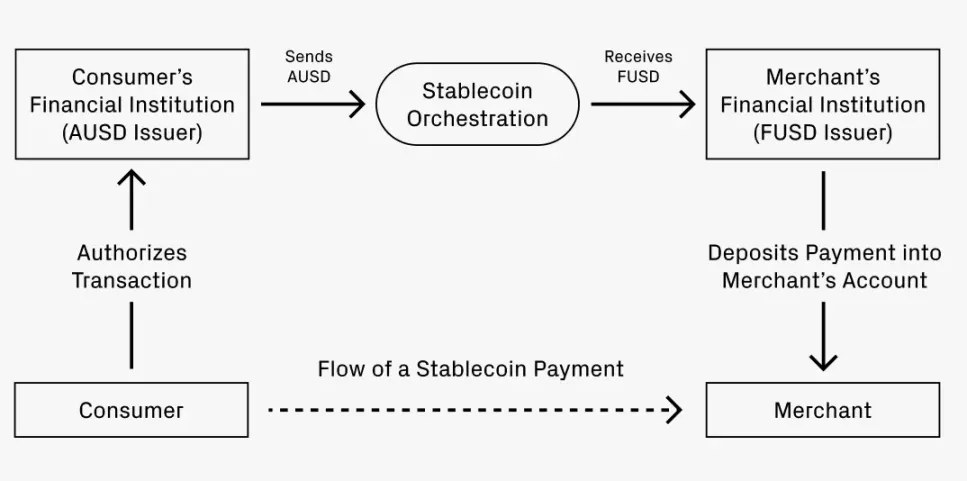

Now, suppose you want to pay with a stablecoin. Your Bank A issues stablecoin AUSD, while the restaurant’s bank, Bank F, only accepts FUSD. How does the payment convert from AUSD to FUSD?

The process closely mirrors the credit card transaction:

- Bank A authorizes the transaction for AUSD.

- A coordination service facilitates the conversion from AUSD to FUSD, potentially charging a small fee. There are several ways this conversion might occur:

- Path 1: Using decentralized exchanges for stablecoin swaps, such as Uniswap, with fees as low as 0.01%.

- Path 2: Converting AUSD to a dollar deposit, depositing it with the acquiring bank, and issuing FUSD.

- Path 3: Coordinating a net settlement of funds through a network, which may require a certain scale to execute effectively.

- FUSD is deposited into the merchant’s account, likely with a service fee deducted.

When Does the Analogy Become Distinct?

The similarities between credit card networks and stablecoin frameworks suggest when stablecoins might significantly upgrade and, in some ways, surpass credit card networks.

Firstly, consider cross-border transactions. If the earlier scenario involves a U.S. consumer paying at an Italian restaurant, the consumer wants to pay in dollars while the merchant wishes to receive euros. Existing credit cards may charge fees up to 3%. In contrast, exchanging stablecoins on a DEX could cost as little as 0.05% (a 60-fold difference). This fee reduction applied to broader cross-border payments makes the productivity gains for global GDP clear.

Secondly, the speed of payment flows from businesses to individuals is rapid: once authorized, funds can exit an account immediately. Instant settlement is both valuable and highly anticipated. Many businesses have global workforces, leading to potentially more frequent and larger cross-border payments than typical consumer transactions. As the workforce continues to globalize, this will provide strong momentum for stablecoin adoption.

Future Opportunities: Where Might They Arise?

If the analogy between network structures holds any value, it could reveal areas where entrepreneurial opportunities may emerge. Established firms in the credit card ecosystem have evolved through payment coordination, issuance innovation, and support for various formats. A similar evolution may occur with stablecoins.

The previous examples primarily illustrate the role of payment coordination, as the flow of funds represents a massive business. Companies like Visa, Mastercard, American Express, and Discover boast valuations in the hundreds of billions, collectively exceeding $1 trillion. Their ability to maintain balance in the market indicates healthy competition and a sufficiently large market to support significant enterprises. It is reasonable to speculate that the stablecoin coordination space will see similar competition as it matures. With stablecoins only around 1 to 2 years into infrastructure development, there remains ample time for new startups to seize these opportunities.

Issuing stablecoins is also an area ripe for innovation. Similar to the rise of business credit cards, we may witness more companies wanting to create their own stablecoins. Mastering the payment unit can give companies greater control over end-to-end accounting processes, from expense management to handling foreign taxes. These efforts might form direct business lines for stablecoin coordination networks or inspire entirely new startups, much like Lithic.

The issuance of stablecoins could also become more specialized. In credit cards, many allow customers to pay upfront fees for enhanced reward structures, such as Chase Sapphire Reserve or AmEx Gold. Some companies, typically airlines and retailers, even offer proprietary credit cards. It wouldn’t be surprising to see similar experiments with stablecoin rewards tiers emerge, opening new avenues for startups.

All these trends drive mutual growth. As issuance formats diversify, the demand for payment coordination services will increase. As coordination networks mature, they will lower the barriers for new issuers to enter the market. These present enormous opportunities, and I look forward to seeing more startups entering this space. In the long run, it could be a multi-trillion-dollar market capable of accommodating multiple large players.

-

-

-

-

-

-

-

-