I have a deep passion for Web3 gaming, with a significant portion of my investments in game NFTs and tokens. However, I remain highly skeptical about pure game tokens.

The Need for Market Normalization

Currently, I have little faith in game projects that have lost momentum since their Token Generation Events (TGEs). If I were a trader, I’d see more promise in those trading Memecoins or betting on the booming AI sector.

Right now, there’s little justification for placing large bets on game tokens, as the market reflects this reality. There are various reasons for this, but primarily it boils down to the lack of critical factors supporting inflated market valuations.

1. Overvaluation of Game Tokens

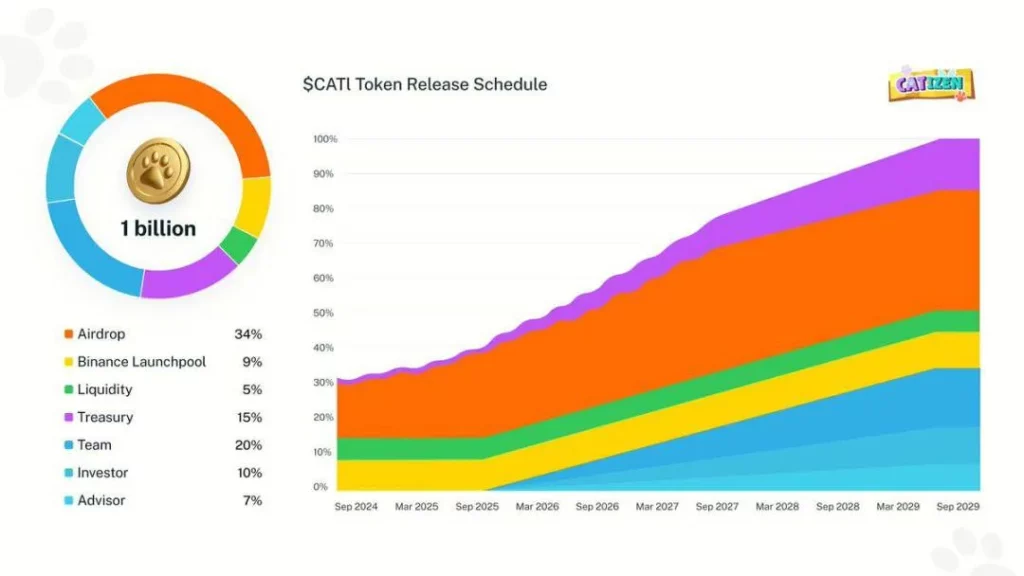

Few Web3 games can justify their market valuations. Even when considering market cap rather than fully diluted valuation (FDV), many games are still overpriced. For instance, CATIZEN is one of the standout games with a market cap of about $200 million, assuming annual revenue of $20 million.

To illustrate, consider a comparison to stocks: South Korean game company Shift Up recently went public with a market cap of $2.4 billion and 2023 revenue of $140 million. The market perceives it as overvalued due to its potential.

In contrast, Nexon has a market cap of $16.3 billion with $3 billion in annual revenue, while Krafton stands at $12.3 billion with $1.5 billion in revenue. Typically, large gaming companies see annual profits constituting 10-20% of their market cap.

CATIZEN appears to be a healthy project at first glance, but the unlock mechanisms present a challenge. Traditional gaming companies require financing to scale, while Web3 game tokens unlock automatically.

In reality, pure game projects without a robust infrastructure are unlikely to grow. Most games experience initial user spikes at launch, followed by gradual declines—an industry norm. The idea that Web3 games can self-appreciate contradicts market principles.

2. Memecoins Are More Attractive

The ability to identify low-cap gems in trading is a valuable skill, and the simplest indicator is trading volume. Low trading volumes indicate a lack of market interest, leading to weak upward momentum. Who wants to trade in a sector that has been declining since its inception?

Comparing the charts of NEIRO, CATI, and HMSTR on Binance shows a clear difference. While CATI outperforms traditional Web3 games in revenue and social media engagement, its market performance is lackluster. The trading volume of NEIRO and CATI differs by about tenfold on Binance.

Given the current market sentiment and the appetite for exchange listings, this is one of the worst times for game tokens to undergo TGEs. Gaming is inevitably driven by venture capital, and projects that cannot compete will quickly exit through NFT sales or TGEs.

Thus, trading and holding Memecoins can be more advantageous than holding game tokens.

I believe three principles determine stock prices: expectations of a company’s future value, its performance history, and fluctuations in market supply and demand. Right now, game tokens lack performance history and are oversupplied, making their competitiveness as pure games unreliable without unique marketing strategies.

While comparing game tokens to stocks isn’t entirely appropriate, it does offer some insight. The key is identifying which projects can drive market narratives. If a company’s future value hinges solely on its game, it may struggle to survive. It needs infrastructure and technological momentum.

Alternatively, unlocking all tokens at once could allow the market to determine the price.

Final Thoughts

I believe the cryptocurrency market will see significant growth in Q1 2025. Like many, I love Web3 games, but I feel that the FDVs of pure Web3 game tokens need to decrease. If you have infrastructure or a technological moat (like a gaming chain), you can command a higher valuation. However, many highly valued games currently only serve the gaming sector.

This could be the worst time for game projects, or it might signify a normalization process. I’ve participated in several rounds of KOL funding for game projects this year, most of which are unprofitable. VC involvement has driven FDVs higher, and the token lock structures defy average market principles.

Nevertheless, some game projects will survive this process, and we should focus on those that can scale into platforms and infrastructure based on revenue. Remember, market movement is often driven by a couple of giants, and we are positioned ahead of traders, allowing us to choose the leading projects first. However, our weakness may be an obsession with the gaming future. Even though we love games, we must try to commercialize them effectively.

-

-

-

-

-

-

-

-