The core function of blockchain networks is to securely process and maintain timestamped information records. In principle, blockchains can record any type of data, but most typically, they handle information related to financial balances and transactions. The simplest and most common financial transaction is payment.

While blockchains currently serve various use cases, the fundamental use case for all major networks remains the transfer of value units (e.g., payments for goods or services). Despite their success in niche markets as dominant payment networks, blockchains’ success in everyday, large-scale payments often stems from stablecoins pegged to fiat currencies.

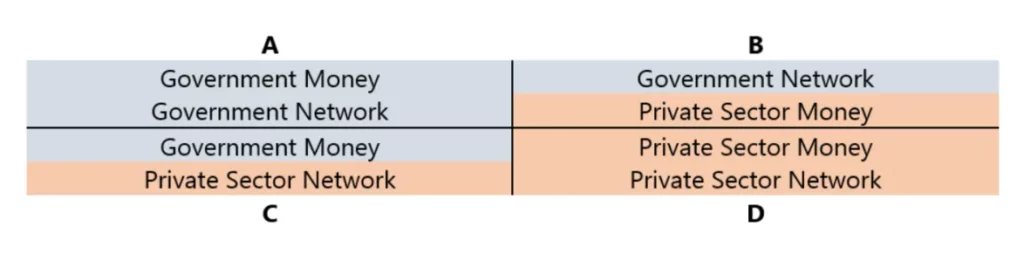

Currency and payment networks can be either public or private. “Public” refers to entities like governments, central banks, and other public sector institutions, while “private” refers to privately owned and operated entities, such as most commercial banks, credit card companies, and other financial service providers.

In practice, the distinction between public and private is not as clear-cut as shown in the diagram’s quadrants. Government-issued public money circulates within private networks, and many private financial sectors are heavily regulated by public institutions.

However, the public-private distinction provides a good starting point for understanding the relationship between emerging currencies and payment systems and existing ones.

Below, we explain and illustrate this table in two cases:

- Covering all monetary units of account.

- Within government-defined units of account, typically tied to national currencies.

In the first case, a currency can only be considered truly “private” if it is issued by private sector entities, uses a unit of account different from government-defined ones, and is traded independently of government-controlled settlement networks.

Free-floating cryptocurrencies like Bitcoin and Ethereum fall into this category of private currencies, though their use as units of account and payment media is quite limited, such as for blockchain transaction fees, NFTs, and other blockchain-related goods and services.

Due to the powerful network effects of national currencies, private currencies outside of cryptocurrencies have similarly limited use cases in everyday payments.

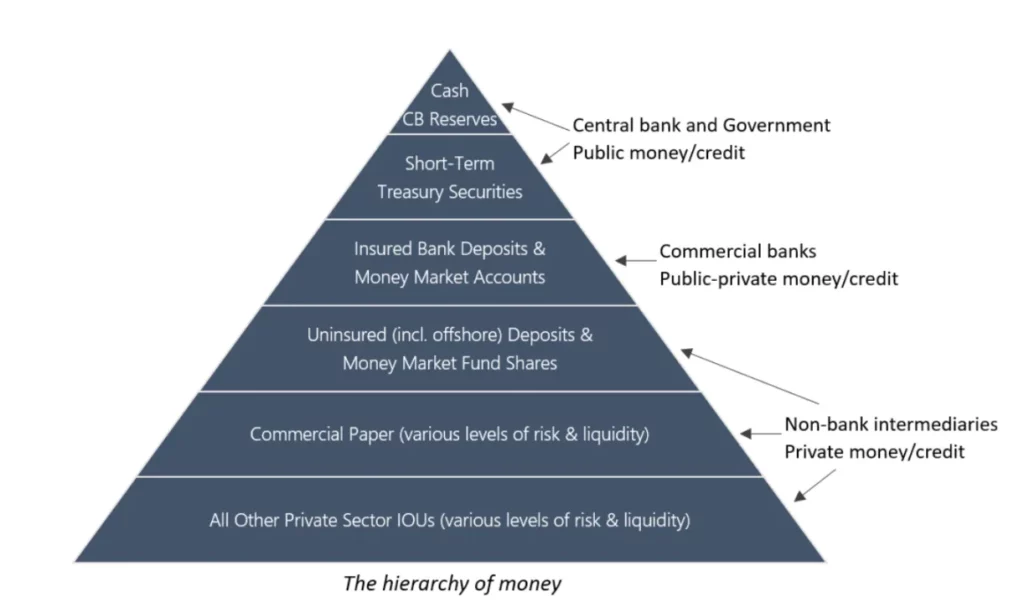

In the second case, currencies tied to national currencies can also take more “public” or more “private” forms. This can be illustrated by the classic hierarchy of money, where acceptance and liquidity decrease from top to bottom: the most accepted and liquid (public) money is at the top, while the least (private) money is at the bottom.

While regional and historical differences may exist, the diagram roughly reflects the situation in most modern economies, where the right to issue money is limited to central banks. The associated monetary units are then used by commercial banks, non-bank financial intermediaries, and private sectors to price credit and securities, which are considered cash equivalents to varying degrees.

Although the most widely adopted private currencies (including free-floating cryptocurrencies) may develop their own independent monetary hierarchies, national currencies and their hierarchies dominate payment use cases worldwide.

This is relevant to blockchains because their success as large-scale payment networks seems increasingly linked to a specific set of cryptocurrencies within the same monetary hierarchy as government currencies. These cryptocurrencies, known as stablecoins, aim to track the market value of other assets.

As of this writing, the most widely pegged asset for stablecoins is the US dollar, the world’s most liquid fiat currency. Therefore, most stablecoins effectively fall within the monetary hierarchy of the US Federal Reserve System.

Payment networks serve different retail and institutional customer groups and use various settlement media (e.g., private IOUs, commercial bank deposits, central bank reserves) across different levels of the dollar hierarchy.

For example, large interbank transactions are processed through Fedwire and the Clearing House Interbank Payments System (CHIPS), while smaller transactions, such as utility bill payments or transfers between family and friends, are handled by the Automated Clearing House (ACH). The most popular point-of-sale payment methods are debit/credit cards, usually issued by banks and linked to mobile payment apps.

Currently, the largest networks processing such payments are operated by publicly traded companies like American Express, Mastercard, and Visa. Lastly, payment gateways like PayPal, Square, and Stripe provide merchants with convenient online access, simplifying the connections between different parts of this system.

At each level of the monetary hierarchy, control over the payment network includes the power to decide what constitutes acceptable means of payment. This is why accounting conventions are so important. Generally, as one moves down the hierarchy, “issuing money” becomes easier, but getting others to accept it becomes harder.

On the one hand, physical cash and commercial bank deposits are almost universally accepted as means of payment, but the ability to issue these forms of money is heavily regulated. On the other hand, virtually anyone can freely issue private debt, but such IOUs function as money only within a very limited scope, such as gift cards or loyalty points issued by specific enterprises. In short, not all forms of monetary payments are created equal.

How do dollar stablecoins settled on blockchain networks fit into this system? From a unit of account perspective, dollar stablecoins can be said to reside in quadrant C of the diagram. Although issued by private sector entities, they are not truly private currencies like Bitcoin and Ethereum due to their peg to the dollar.

This is particularly true for stablecoins backed by USD deposits or cash equivalents (or even physical commodities) held by regulated US financial institutions, making them slightly higher in the hierarchy than stablecoins backed by offshore assets.

However, both ultimately fall into the same broad category, below insured bank deposits. Stablecoins backed entirely by free-floating cryptocurrencies are a special case, as their association with the existing financial system is lower. However, when explicitly designed to peg to the dollar’s value, these stablecoins can still be classified in quadrant C.

From the perspective of government-defined units of account (the dollar), anything other than physical currency and reserve money held by central banks constitutes liabilities of private sector entities, and thus can be classified as “private” money. From this viewpoint, given that all such liabilities (including stablecoins) also circulate within privately operated payment networks, they can be said to reside in quadrant D.

Although there are significant quality differences between stablecoins depending on the issuer and the location of their primary banking partners, the increasingly popular notion that “on-chain is the new offshore” highlights the similarities between stablecoins and offshore dollars (i.e., “Eurodollars”), which are not under direct regulation by US authorities.

Even if the assets backing stablecoins are held by US-regulated financial institutions, from the holder’s perspective, they still represent dollar liabilities lacking the insurance of government-guaranteed bank deposits. While the counterparty and financial risks associated with specific stablecoins may vary, they ultimately place them in the same category as all other privately issued dollar-denominated debt forms lacking guarantees, though still regarded as money.

Stablecoins, however, have a unique feature: they are issued on decentralized, programmable blockchains. This means anyone with a connected device can register a self-custody digital wallet without authorization, receive peer-to-peer transfers globally at low cost, and access blockchain-based financial services.

In other words, the innovative part of stablecoins is not the currency itself but the technology and distribution. Because of their native digital nature, global reach, and programmability, stablecoins have the potential to become a more powerful and convenient form of digital cash than any currently existing currency. What are the main barriers to realizing this potential? Consider three possible scenarios for stablecoin adoption in everyday payments:

Niche/Marginalized

Stablecoins achieve the highest adoption rates in certain niche markets (crypto-native and traditional) and special situations (e.g., currency crises or regions with highly underdeveloped or dysfunctional financial services infrastructure), remaining marginal in global everyday payments.

In most developed economies, existing payment methods such as debit/credit cards, non-crypto mobile wallets, and even physical cash are highly convenient and reliable, with little demand for alternative payment methods.

Without strong consumer demand, stablecoin payments may struggle to enter broader economic realms. This is especially true if stablecoins face adverse regulatory treatment in major jurisdictions, hindering their use as alternatives or supplements to traditional bank deposits.

Mainstream/Fusion

As stablecoins integrate closely with existing payment infrastructures, blockchain-based and traditional financial services will gradually merge. Clear regulatory support for crypto attracts established financial institutions (especially banks) to issue or otherwise support stablecoins, increasing trust in the underlying blockchains.

As the lines between stablecoins and traditional bank accounts blur, a unified regulatory framework will eventually emerge, consolidating blockchains as a core component of global financial infrastructure through embedded, increasingly automated compliance regimes. Major stablecoin issuers will become significant financial institutions, though their risk profiles will vary based on their architecture and regulatory status.

Thus, in the event of a significant financial crisis, some of these institutions may falter, posing challenges for governments and central banks similar to those faced after the 2007-2008 global financial crisis, further solidifying their roles as lenders and market makers of last resort.

Meanwhile, blockchain transparency and programmability will enhance financial sector stability and resilience, paving the way for future national currency reforms and ultimately leading to central bank digital currencies (CBDCs) managed by governments or through public-private partnerships.

Alternative/Disruptive

Stablecoins and blockchain-based financial services will develop parallel to the existing financial system. Over time, blockchains will become less integrated with traditional financial institutions and payment infrastructure, increasingly seen as a systemic alternative, directly competing with and ultimately replacing the traditional system.

Existing institutions will adapt by launching their own blockchains, but many will compete with more native crypto counterparts. Given the unique features and risk profiles of blockchain-based financial services, most jurisdictions will prefer to create entirely new regulatory frameworks rather than attempting to fit them into existing regulations.

While stablecoins pegged to national currencies will remain the primary currency form for most on-chain payments, cryptocurrencies not pegged to existing currencies but maintaining sufficiently stable exchange rates with a basket of consumer goods will eventually emerge.

In the long run, the most disruptive outcome would be these cryptocurrencies being widely adopted for everyday commerce and even international trade, establishing a new monetary system requiring a new global monetary governance institution.

Historically, most cryptocurrencies have exhibited significant price volatility, making them unsuitable as units of account and general payment means. Stablecoins address this issue, arguably making them one of the most successful blockchain use cases to date.

While tokens specific to certain networks and applications have important utility for operators, developers, and managers, their adoption in everyday payments faces higher barriers than stablecoins pegged to off-chain currencies familiar to consumers.

Therefore, regardless of which scenario unfolds, the growth of blockchains as payment networks is closely tied to the success of stablecoins.

-

-

-

-

-

-

-

-