The controversy surrounding exchange listing fees has been heating up, especially after Simon, CEO of Moonrock Capital, posted a complaint about exorbitant listing fees. This sparked a heated debate among key opinion leaders (KOLs) in the industry, raising questions about whether these fees truly exist, what hidden fees might be at play, and how exchanges profit. In the darker corners of the industry, numerous undisclosed transactions may be occurring. Let’s dive into the controversy and uncover what’s happening behind the scenes.

The Exorbitant Listing Fee Controversy

The debate over high listing fees has drawn significant attention since it first emerged. Several industry figures have weighed in on the issue, with notable responses coming from Andre Cronje, co-founder of Sonic Labs, who quickly denied accusations about Coinbase’s listing fees.

TRON founder Justin Sun also weighed in, stating that Binance did not charge any listing fees for their token but that Coinbase had once asked for 500 million TRX (roughly $80 million) and required the deposit of $250 million in BTC in Coinbase Custody to improve performance.

Conflux COO Zhang Yuanjie also chimed in, stating that Binance did not charge any listing fees for Conflux’s CFX token. However, Binance did impose a penalty, seizing a $150,000 USD deposit due to the token’s poor performance. Conflux’s collateral of 5 million CFX tokens was ultimately refunded after the network was found to be secure.

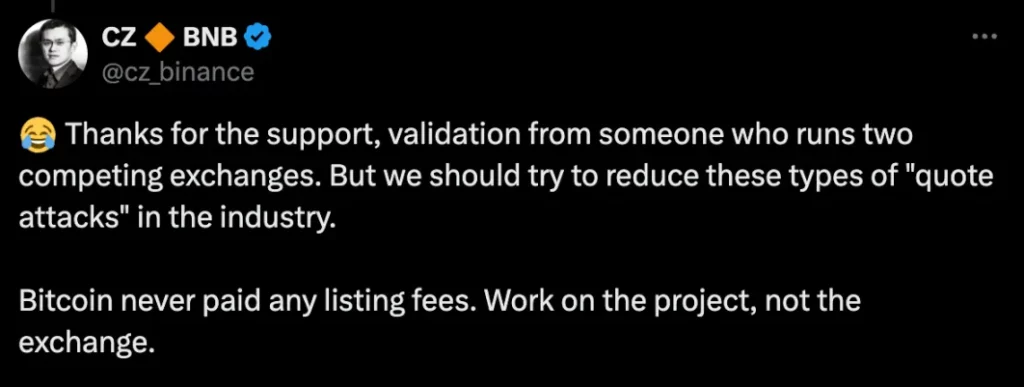

Binance quickly responded, with CEO Changpeng Zhao (CZ) clarifying that Bitcoin has never paid any listing fees. He emphasized that projects should focus on the quality of their tokens, not the exchanges they list on.

What Are the Hidden Listing Fees?

In September, Binance’s He Yi addressed the growing concerns about listing fees, clarifying that Binance operates within a structured and rigorous process. This process involves four stages: business development, research teams, committee review, and compliance checks. There is no suspicion of insider trading or information leakage in their listing process.

While Binance has stated that there is no direct “bribe” in the form of token allocations or stablecoins, project teams are required to allocate a portion of their token distribution (approximately 5%) to Binance’s Launchpool, without any specific airdrop reserved for individual users. Apart from these known fees, the Conflux case highlighted that project teams must provide a substantial security deposit to ensure token price stability, or they risk having it forfeited.

Some argue that the requirement for a security deposit and airdrop allocations are merely different ways of structuring “listing fees” that hide beneath the surface, akin to the tip of an iceberg. Others counter that these are not hidden fees but legitimate incentives meant to reward users.

The Hidden Concerns of Centralized Exchanges

The crypto industry is full of secretive corners, and the lucrative revenues generated by exchanges make it hard to guarantee transparency in all transactions.

Beyond the usual trading fees and interest income, exchanges also profit from smaller, untradeable assets left in user accounts, as well as from arbitrage and off-book transactions. Some non-compliant exchanges even engage in malicious practices such as “spoofing” (placing fake orders to manipulate prices), “data manipulation,” and “news dumping” to exploit market conditions for profit.

In traditional centralized exchanges, the conflicts of interest between project teams, market makers, and exchanges often go unseen by retail investors. This lack of transparency leads to an imbalance where retail traders are at a disadvantage.

For example, during the GameStop (GME) incident, the Robinhood trading platform restricted buys and sells, manipulating stock prices to the benefit of larger investors. Such actions are not isolated and pose a threat to fair market functioning, as retail traders are often caught in the crossfire of exchanges’ profit-seeking strategies.

Negative Listing Return Rates

The ultimate goal of listing tokens is profitability—whether it’s for retail investors, exchanges, or project teams. However, the current return rates from listings paint a troubling picture.

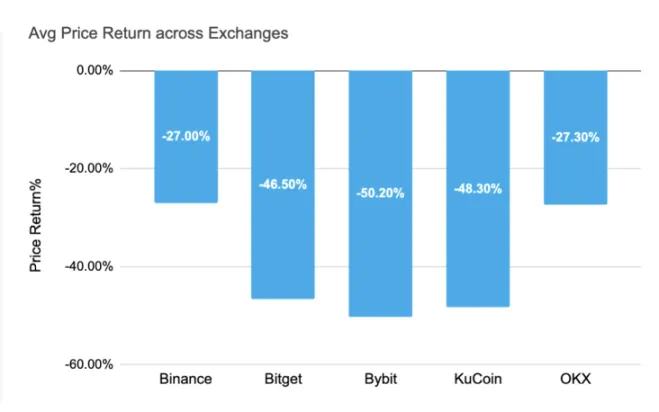

So far in 2024, the average return on newly listed tokens across major exchanges has been negative. Bybit’s average return has dropped the most, with a decline of -50.20%, followed by KuCoin at -48.30% and Bitget at -46.50%. Even Binance and OKX have seen negative returns of -27.00% and -27.30%, respectively. This poor performance suggests that focusing on “hidden listing fees” may not be the most pressing concern. Instead, the industry’s focus should shift to the actual price stability and long-term development of the tokens being listed.

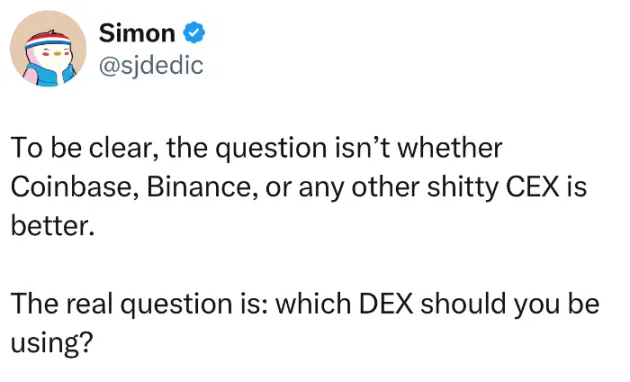

Given these negative return rates, the industry’s ongoing reliance on high fees—whether hidden or not—could limit future growth and hinder long-term sustainability. As Simon, who revealed the issue of exorbitant listing fees, pointed out, the real question is not whether exchanges like Coinbase, Binance, or others are better or worse but rather which decentralized exchange (DEX) to use moving forward.

The Road Ahead for Centralized Exchanges

The debate over listing fees highlights a broader issue with centralized exchanges. While they continue to be major players in the market, their practices often lack transparency, leaving investors to navigate an opaque and sometimes exploitative landscape. This raises important questions about how the industry can evolve to ensure fairness, accountability, and long-term growth.

As the market matures, there may be increasing pressure on exchanges to rethink their fee structures and adopt more transparent, user-friendly models. With growing interest in decentralized finance (DeFi) and decentralized exchanges, these platforms could offer a potential alternative that focuses more on fairness and community-driven growth.

In the end, the discussion about hidden listing fees is just the tip of the iceberg, and the crypto industry must continue to evolve to address these systemic issues. Whether the solution lies in a shift toward decentralized platforms or a reformation of centralized exchanges remains to be seen.

-

-

-

-

-

-

-

-