If you’re interested in Restaking or Active Validation Services (AVS), this article will provide a simple comparison of @eigenlayer, @symbioticfi, and @Karak_Network, along with an introduction to the related concepts, which should be helpful for you.

What are AVS and Restaking?

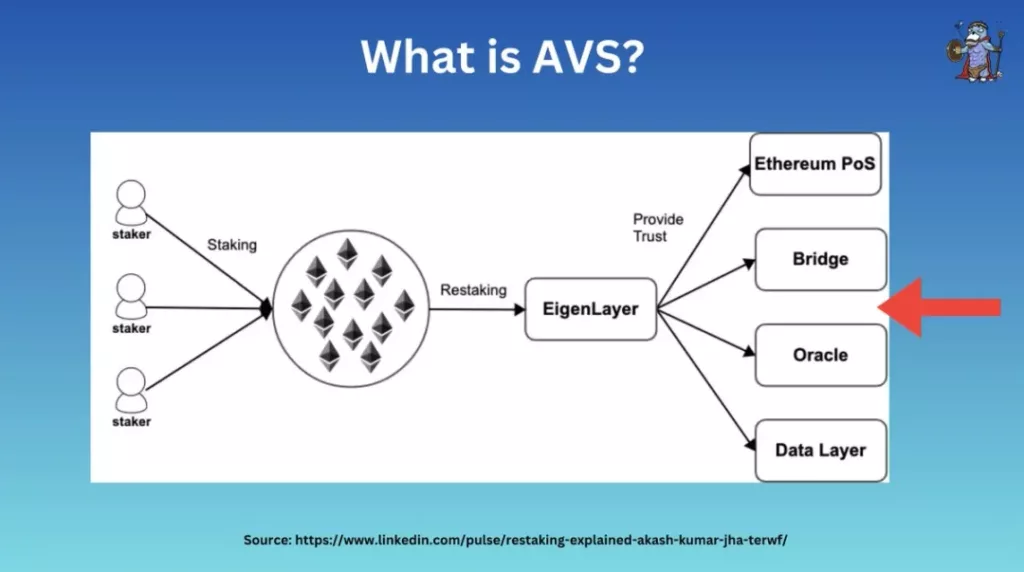

AVS stands for Active Validation Services, a term that essentially describes any network requiring its own validation system (e.g., oracles, DA, cross-chain bridges, etc.).

In this article, AVS can be understood as projects using restake services.

Conceptually, restaking is a method of “reusing” staked ETH for additional validation/services to earn more staking rewards without unstaking.

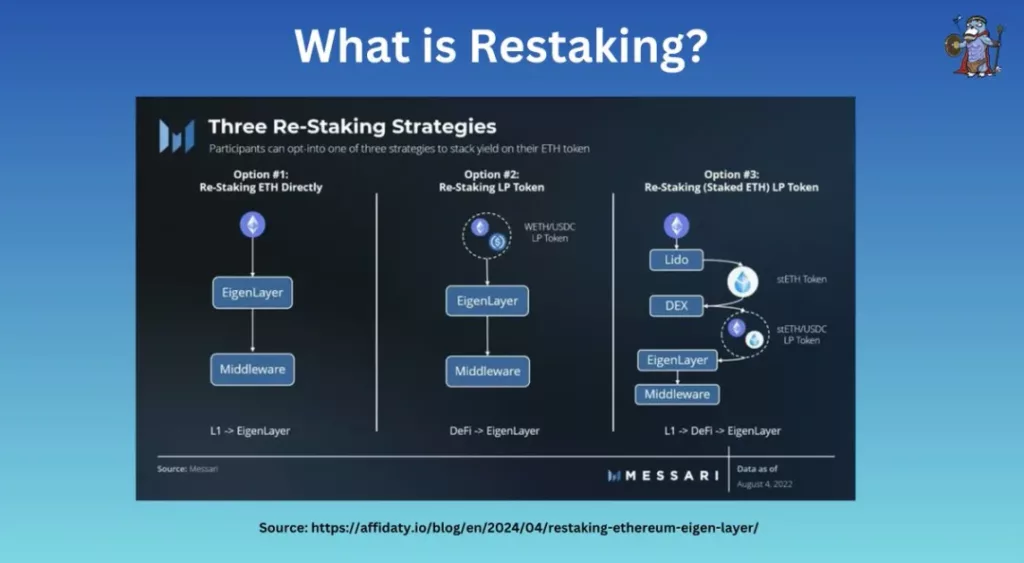

Restaking typically comes in two forms:

- Native Restaking

- LST / ERC20 / LP Restaking

Through restaking, restakers and validators can protect thousands of new services by pooling security.

This helps reduce costs and provides new trust networks with the security guarantees they need to get started.

Among these restaking protocols, @eigenlayer (EL) was the first to launch.

EigenLayer

Key Architecture

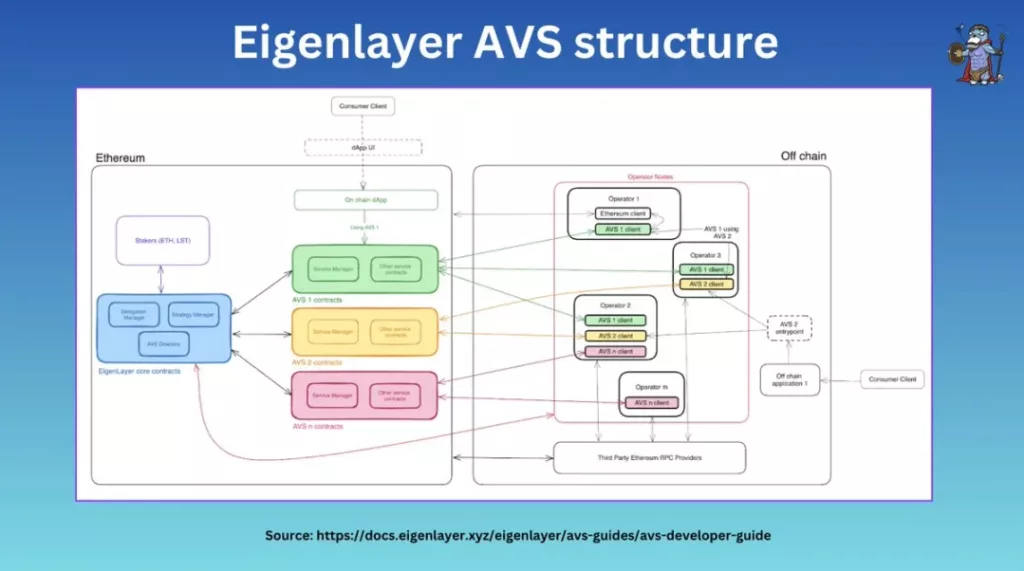

At a high level, @eigenlayer (EL) consists of four main components:

- Stakers

- Operators

- AVS contracts (e.g., token pools, designated slasher)

- Core contracts (e.g., delegation manager, slashing manager)

These parties work together to allow stakers to delegate assets and validators to register as operators on EigenLayer.

AVS on EL can also customize their own quorum and slashing conditions.

Restaking

EigenLayer supports both native and liquid restaking.

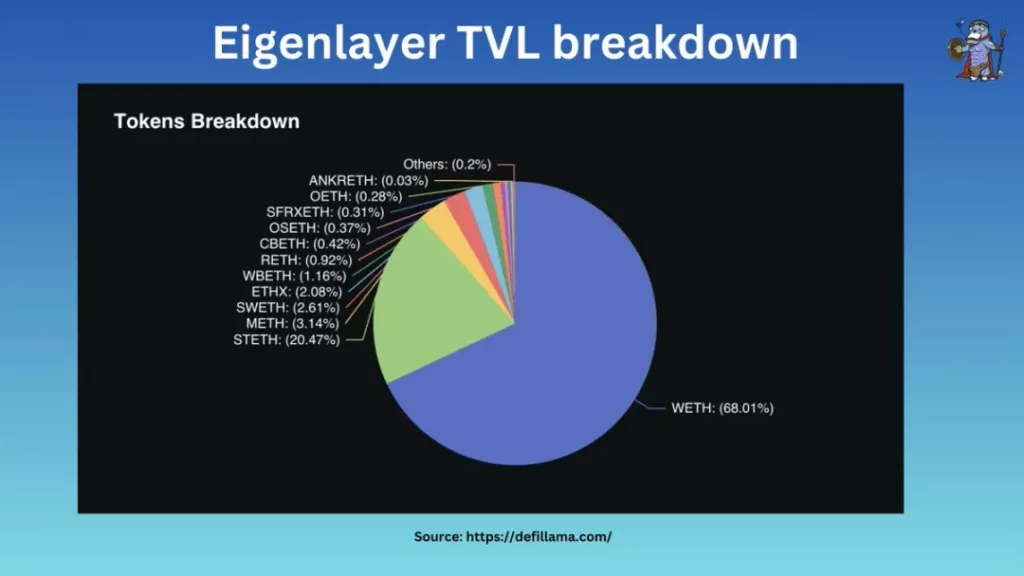

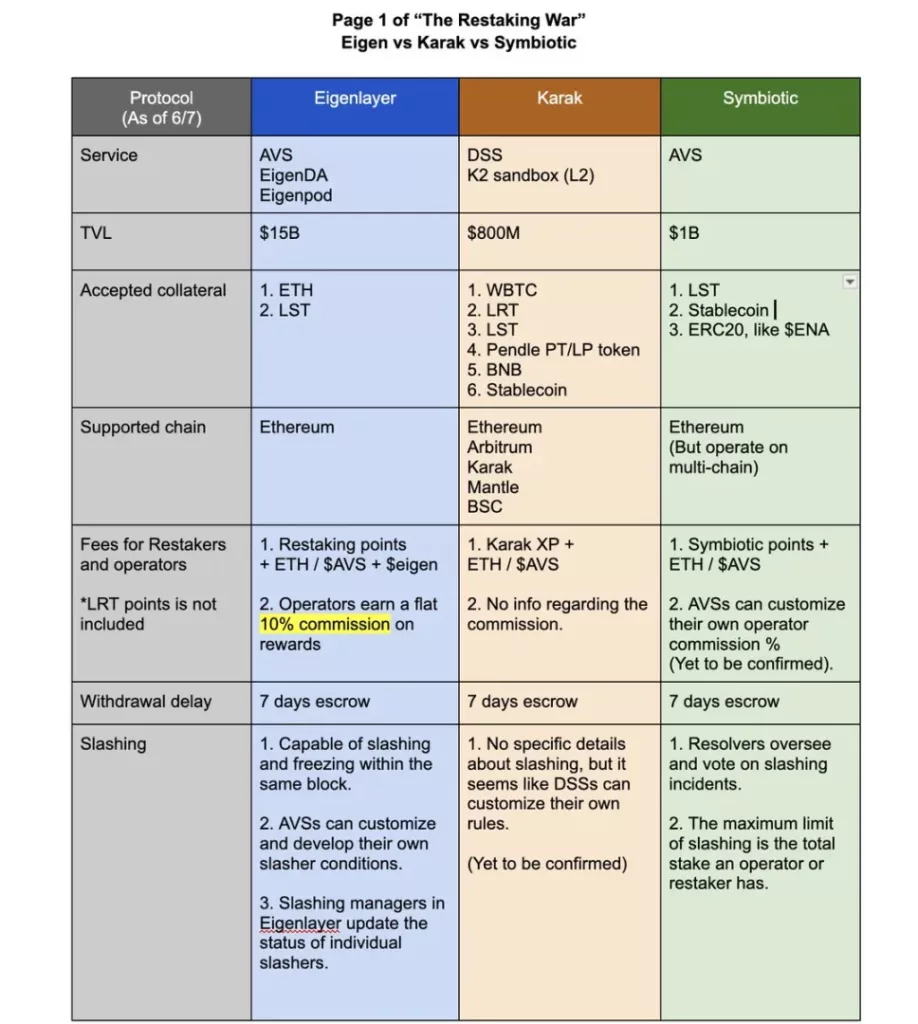

In its approximately $15 billion TVL (Total Value Locked):

- 68% of assets are native ETH

- 32% are LSTs (Liquid Staking Tokens).

EigenLayer has around 160,000 restakers, but only about 1,500 operators, with 67.6% (around $10.3 billion) of assets delegated to operators.

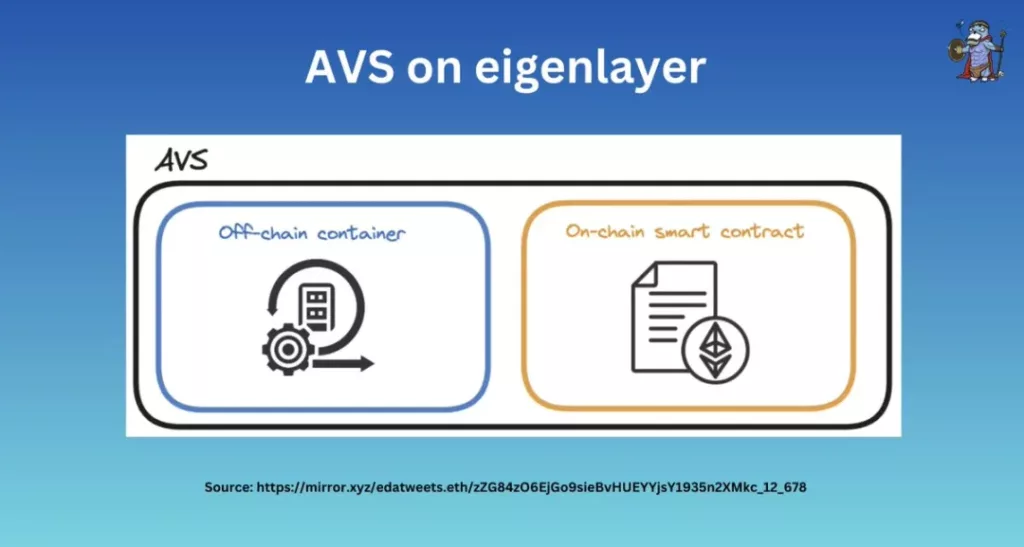

AVS on EigenLayer

EigenLayer offers high flexibility for AVS self-design, allowing them to determine:

- Staker quorum (e.g., 70% ETH stakers + 30% AVS token stakers)

- Slashing conditions

- Fee model (paid in AVS tokens / ETH, etc.)

- Operator requirements

And their own AVS contracts.

Role of EigenLayer

EL controls:

- Delegation manager

- Strategy manager

- Slashing manager

Validators wishing to become EL operators must register through EL.

Strategy managers are responsible for accounting balances of restaking participants and executing in collaboration with delegation managers.

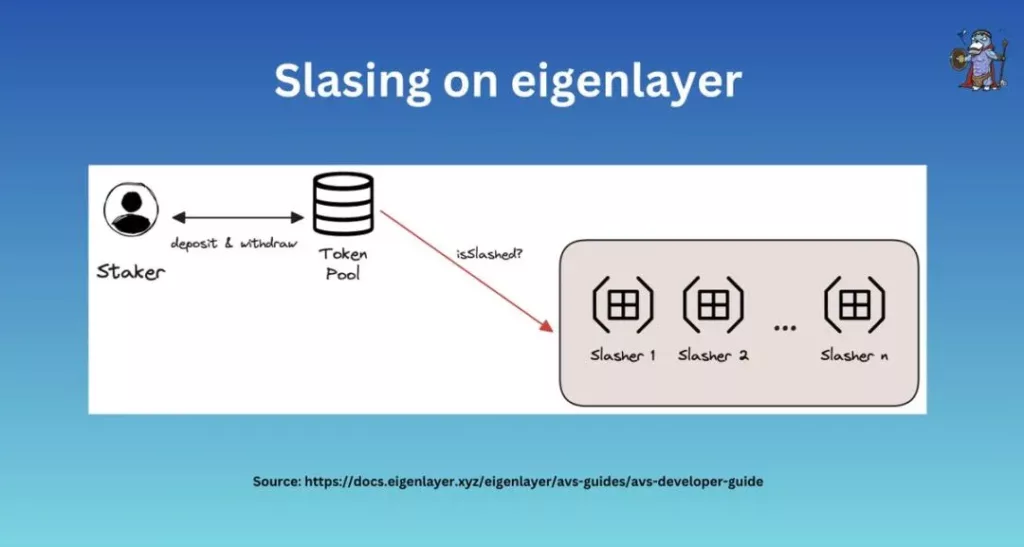

Slashing

Each AVS has its own slashing conditions.

If operators behave maliciously or violate EL commitments, they will be slashed by slashers, each with its own slashing logic.

If operators choose to participate in 2 AVS, they must agree to the slashing conditions of both AVS.

Veto Slashing Committee (VSC)

In the case of “incorrect slashing,” EL has a VSC that can reverse slashing outcomes.

EL itself does not act as a standard committee but allows AVS and stakeholders to establish their own preferred VSC, creating a market for VSCs tailored to different solutions.

Summary

In short, EL offers:

- Native + LST staking

- Asset delegation (ETH assets + EIGEN)

- AVS can highly flexibly design their own terms

- Veto Slashing Committee (VSC)

- Launched operators (about 1,500 as of now)

Symbiotic

@symbioticfi positions itself as a “DeFi hub” for restaking by supporting staking of assets like ENA and sUSDe.

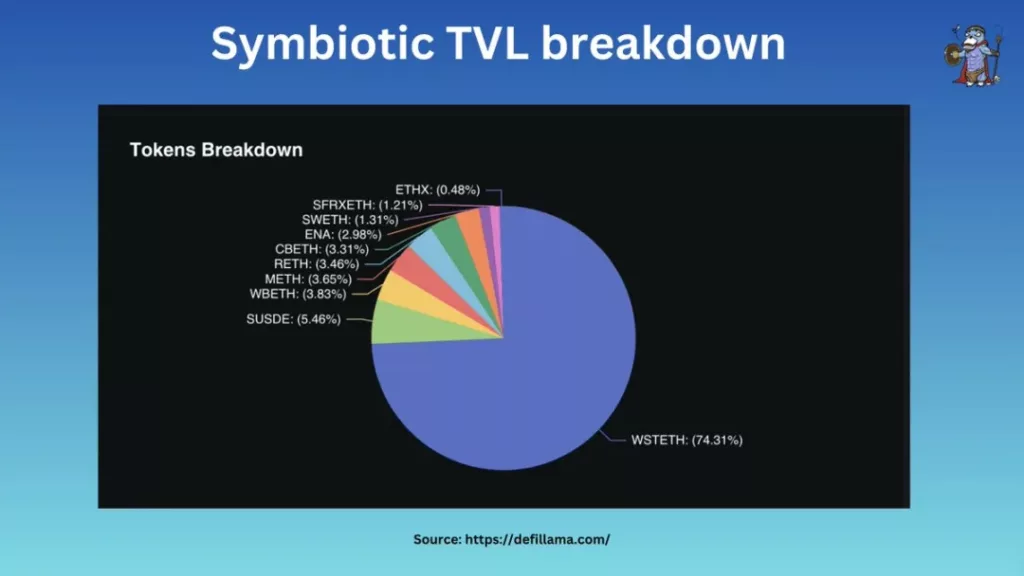

Currently, 74.3% of its TVL is wstETH, 5.45% is sUSDe, with the rest comprising various LSTs.

Native restaking is not yet live but may be supported soon.

Symbiotic ERC20

Unlike EL, @symbioticfi mints corresponding ERC20 tokens to represent deposits.

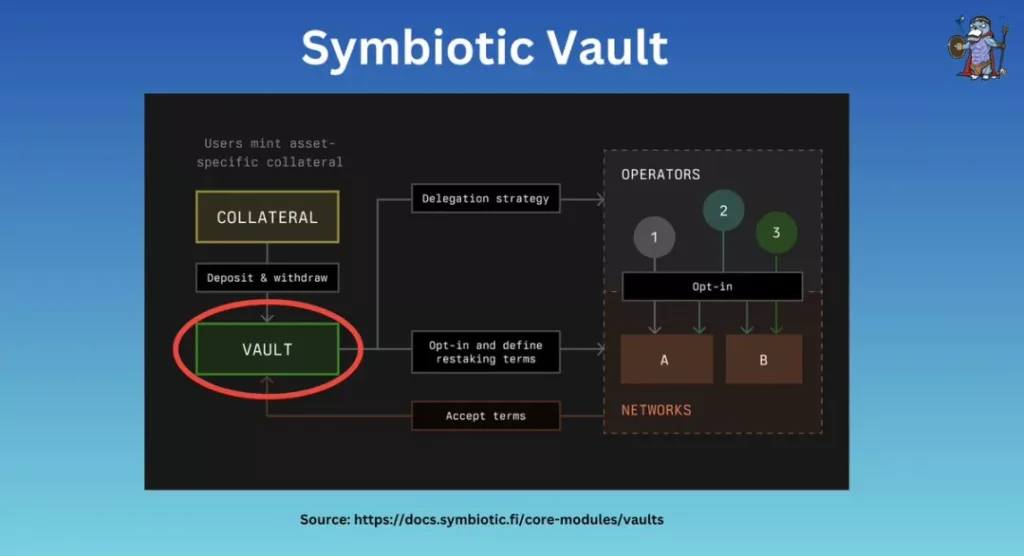

Once collateral is deposited, the assets are sent to a “vault” and then delegated to the respective “operators.”

AVS on Symbiotic

In Symbiotic, AVS contracts/token pools are referred to as “Vaults.”

A Vault is a contract established by AVS, using Vaults for accounting, delegation design, etc.

AVS can customize staker and operator reward processes by integrating external contracts.

Vault

Similar to EL, Vaults can be customized, such as having multi-operator Vaults, etc.

One significant difference with EL is the presence of immutable pre-configured Vaults, which deploy using pre-configured rules to “lock in” settings and avoid the risks of upgradable contracts.

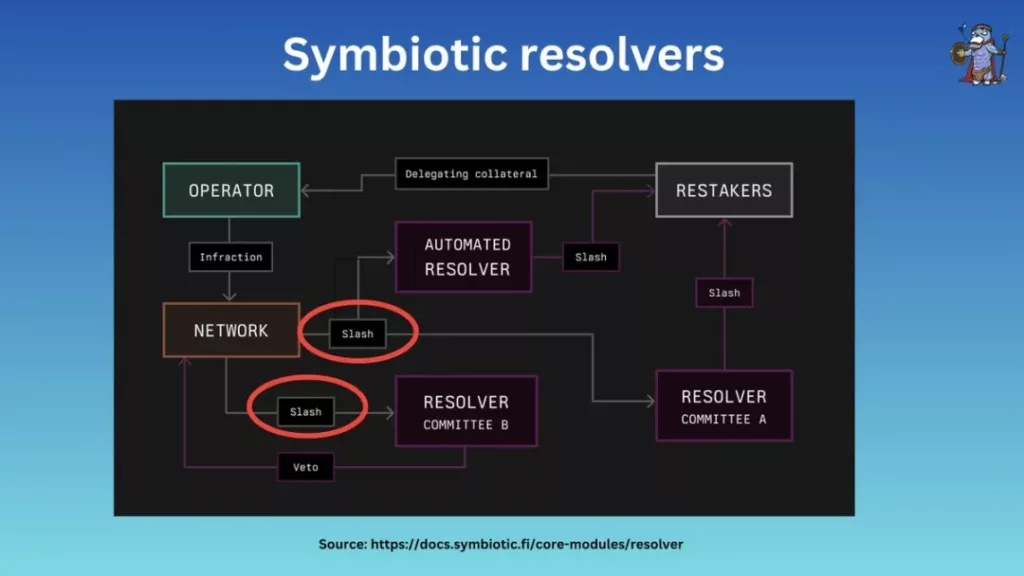

Resolver

Resolvers are equivalent to EL’s Veto Committees.

When incorrect slashing occurs, resolvers can veto the slash.

In @symbioticfi, Vaults can request multiple resolvers to cover staked assets or integrate with dispute resolution solutions (e.g., @UMAprotocol).

Summary

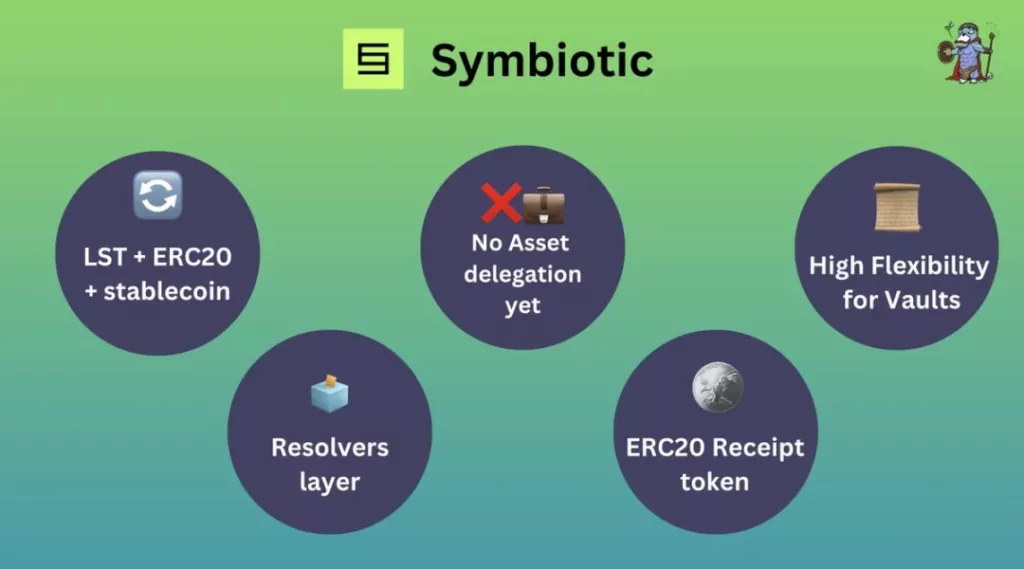

In short, Symbiotic offers:

- Acceptance of LST + ERC20 + stablecoin collateral

- ERC20 receipt tokens minted upon staking

- No native restaking or delegation yet

- Customizable Vaults

- Multi-resolver architecture with higher design flexibility

Karak

Karak uses a system called DSS, similar to AVS.

Among all restaking protocols, @Karak_Network accepts the most diverse range of staked assets, including LST, stablecoins, ERC20, and even LP tokens.

Staked assets can be deposited across multiple chains such as ARB, Mantle, BSC, etc.

Staked Assets

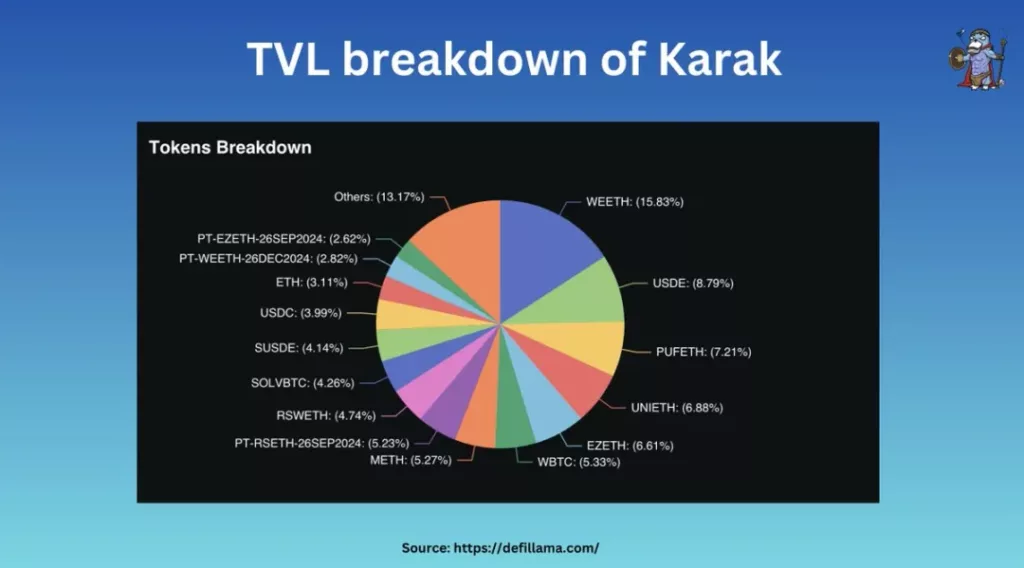

In Karak’s approximately $800 million TVL, most deposits are in LST form, with the majority on the ETH chain.

Simultaneously, about 7% of assets are stored through K2, an L2 chain developed by the Karak team and secured by DSS.

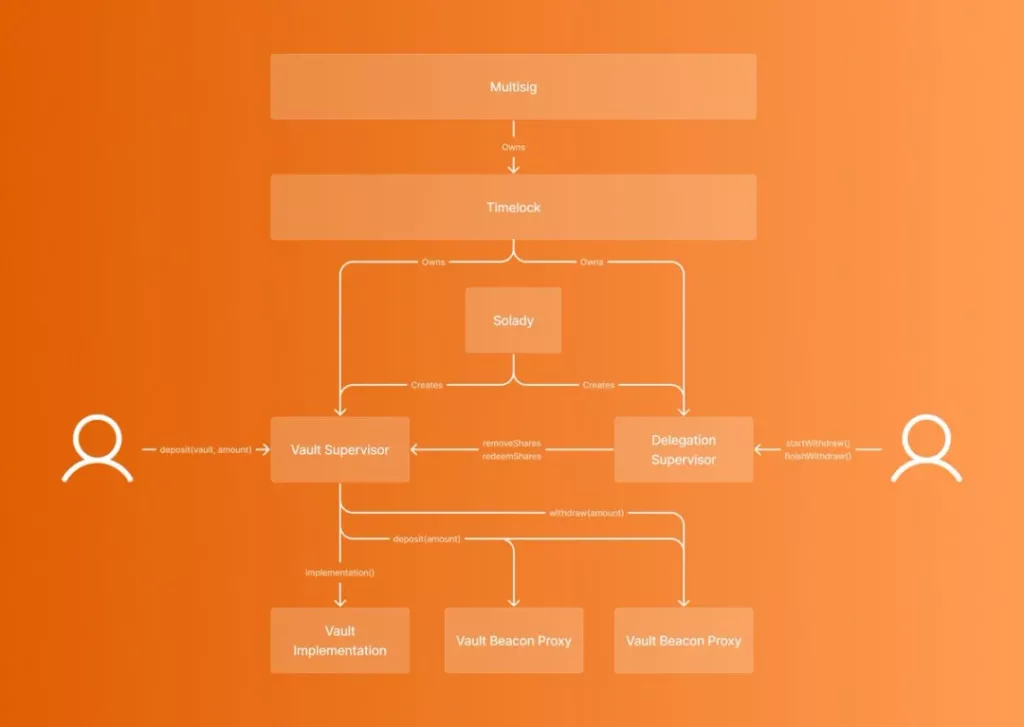

DSS on Karak

So far, Karak V1 offers platforms for:

- Vaults + regulators

- Asset delegation regulators

In terms of architecture, Karak provides a turnkey SDK + K2 sandbox to make development easier.

More information is needed for further analysis.

Comparison

Intuitively, staked assets are the most obvious differentiating factor.

EigenLayer

EL offers native ETH restaking and EigenPods, with ETH accounting for 68% of its TVL, and has successfully attracted about 1,500 operators.

They will soon also accept LST and ERC20 tokens.

Symbiotic

Positions itself as a “DeFi hub” by partnering with @ethena_labs and initially accepting sUSDe and ENA.

Karak

Stands out with its multi-chain staking deposits, allowing restaking across different chains and creating an LRT economy on this basis.

Architecture

Architecturally, they are also very similar.

The process usually goes from stakeholders -> core contracts -> delegation -> operators, etc.

Symbiotic allows multi-arbitration resolvers, whereas EigenLayer does not specify this, but it is also possible.

Reward System

In EL, opted-in operators receive 10% commission from AVS services, with the remainder going to delegated assets.

On the other hand, Symbiotic and Karak may offer flexible options, allowing AVS to design their own payment structures.

Slashing

AVS/DSS are very flexible, allowing customization of slashing conditions, operator requirements, staker quorum, etc.

EL + Sym have resolvers + veto committees to support and recover from incorrect slashing actions.

Karak has not yet announced related mechanisms.

Tokens

So far, only EL has launched a token, EIGEN, requiring stakers to delegate tokens to the same operators as restaking (but they are non-transferable).

Speculation on SYM and KARAK tokens is also a key incentive driving their TVL.

Conclusion

Among these protocols, it is clear that @eigenlayer offers the most mature solution, with the strongest economic security + ecosystem.

AVS seeking security at the start-up stage will build on EL, given its $15 billion pool of funds and 1,500 operators ready to join + top-notch team.

On the other hand, @symbioticfi and @Karak_Network are still in very early stages, with much room for growth. Retail or investors seeking returns on assets beyond ETH/multi-chain assets may opt for Karak and Symbiotic.

Bottom Line

Overall, AVS and restaking technology eliminate the burden of building underlying trust networks.

Now, projects can focus on developing new features and better decentralization.

Restaking is not just an innovation but a new era for ETH.

-

-

-

-

-

-

-

-