In recent days, both the U.S. stock and crypto markets have been dazzled by MSTR (MicroStrategy). During the latest surge in Bitcoin prices, MSTR not only led the rally but also maintained a growing premium over Bitcoin, with its price skyrocketing from around $120 just a couple of weeks ago to the current $247.

While most market participants interpret MSTR’s surge as “leveraged Bitcoin,” this explanation fails to account for why its premium has suddenly spiked despite the fundamental strategy of “debt-to-buy-crypto” remaining unchanged. After all, MicroStrategy has been acquiring Bitcoin for years without such a drastic premium increase.

In reality, the recent spike in MSTR’s premium can be attributed not only to the “debt-to-buy-crypto” strategy but also to another secret weapon of MicroStrategy, which has had a significant impact on its fundamentals. Many analysts have even referred to this as MicroStrategy’s “infinite money-printing machine,” making MSTR “worth more the more it sells.”

Leveraged Bitcoin? An Old Story

MicroStrategy, a company focused on business intelligence software, adopted an aggressive strategy in 2020: raising funds through debt to purchase Bitcoin. This strategy began in August 2020 when the company announced it would convert $250 million of its treasury reserves into Bitcoin. The underlying motivation for this strategy was to address challenges such as declining cash yields and the depreciation of the dollar due to global macroeconomic factors.

To further expand its Bitcoin holdings, MicroStrategy financed itself through the issuance of long-term bonds in the capital markets. These bonds typically have long maturities, many due in 2027-2028, with some being zero-coupon bonds. This allowed the company to maintain low financing costs in the coming years and quickly use the bond proceeds to buy Bitcoin, directly adding to its balance sheet.

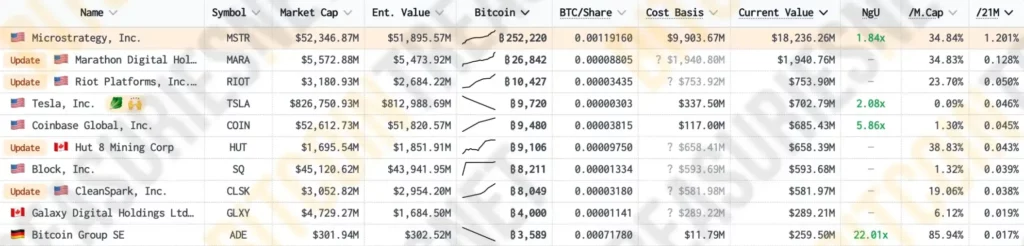

According to data from Bitcoin Treasuries, MicroStrategy currently holds 1.2% of the total circulating supply of Bitcoin, making it the publicly traded company with the largest Bitcoin holdings, far exceeding more “crypto-native” companies like Marathon, Riot, and leading crypto exchange Coinbase.

Through debt financing, MSTR has continuously increased its Bitcoin holdings, which not only boosts the number of Bitcoin on its balance sheet but also exerts a noticeable influence on Bitcoin’s market price. As Bitcoin’s proportion in MSTR’s portfolio has risen, the correlation between the company’s stock market value and Bitcoin prices has strengthened. According to MSTR Tracker, the correlation coefficient between MSTR’s stock price and Bitcoin price recently surged to 0.365, reaching an all-time high.

This correlation encourages investors who are bullish on Bitcoin to also buy MSTR stock, further driving up the company’s market value. However, after four years of market and time testing, MSTR’s “leveraged Bitcoin effect” has become a well-worn topic. Whenever MSTR’s price rises, people instinctively explain it with the “debt-to-buy-crypto” logic.

Yet, during the recent Bitcoin surge, MSTR’s market price not only rose ahead of Bitcoin but also maintained an increasingly high premium over it for some time. This left many investors puzzled: Why did the premium suddenly spike when the fundamentals hadn’t changed?

Premium Increase: “Worth More the More It Sells” – MSTR’s Cheat Code

Let’s first examine just how exaggerated MSTR’s recent premium has been. According to MSTR Tracker, MSTR’s premium over Bitcoin saw a sharp increase earlier this year, rising from approximately 0.95 to 2.43 before falling back to around 1.65. The second rapid increase began just before Bitcoin’s price surge, climbing from 1.84 to a peak of 3.04, currently hovering around 2.8.

Despite MicroStrategy accumulating Bitcoin for the past four years, its NAV (Net Asset Value) premium has not shown significant growth, remaining around 1:1 for an extended period.

So what caused MSTR’s premium to soar? Has the fundamental strategy of “debt-to-buy-crypto” changed?

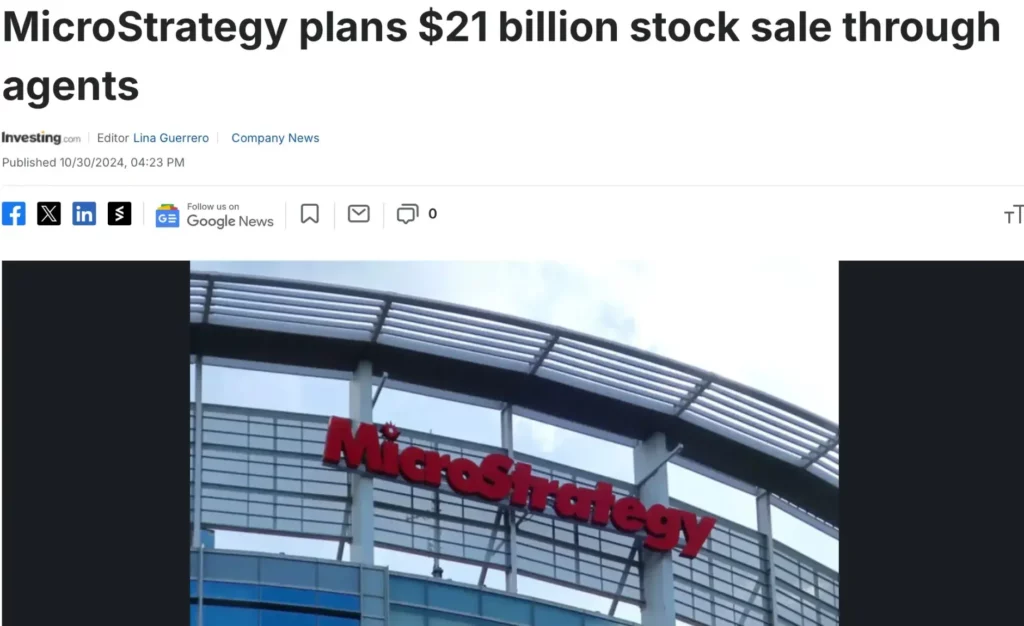

The answer is yes. This fundamental change is known as “premium issuance.” Since late last year, MicroStrategy has adopted a new method for purchasing Bitcoin: issuing and selling additional MSTR shares to buy more Bitcoin. At first glance, this “sell shares to buy Bitcoin” strategy may seem foolish, as it could damage the stock price and potentially threaten MSTR’s market positioning as a “leveraged Bitcoin” asset.

However, when you analyze the logical chain closely, you’ll find that this “sell shares to buy Bitcoin” model is essentially MSTR’s super flywheel and its infinite money-printing machine.

First, let’s clarify the concept of “asset net value premium” (NAV). Since MSTR holds a significant amount of Bitcoin through debt, and with strong market expectations for Bitcoin’s future rise, MSTR’s stock value often exceeds the value of the Bitcoin it holds. This premium is known as the “asset net value premium,” reflecting market expectations for the company’s future Bitcoin holdings expansion and serving as a foundation for MSTR’s continuous stock issuance to acquire more Bitcoin.

On the other hand, when Bitcoin prices rise, MicroStrategy’s market value also increases, forcing various index funds to consider increasing their purchases of MSTR based on weight, further pushing its price and market value up.

At this point, due to the existence of the “asset net value premium,” MSTR can initiate its “premium issuance” operations. By continuously issuing new shares, it gains more funds to buy Bitcoin, driving Bitcoin prices up, which in turn enhances the company’s market value and financing ability, allowing this cycle to continue. This strategy creates a “reflexive flywheel effect.”

The most ingenious aspect of MicroStrategy’s “reflexive flywheel effect” is that the issuance of new shares does not negatively impact MSTR’s price; rather, it makes MSTR more valuable.

When MicroStrategy issues new shares to purchase Bitcoin, the newly issued shares typically trade at a price higher than their NAV. With this premium, MicroStrategy can acquire more Bitcoin than what each share of MSTR truly represents when sold.

For instance, based on the correlation coefficient between MSTR and Bitcoin, 36% of the value of each MSTR share represents the Bitcoin endorsed by the company. Without any premium, when MicroStrategy sells MSTR shares, it would only be able to exchange for 36% of Bitcoin from the market. However, currently, MSTR’s premium over Bitcoin is around 2.74, meaning that each time MicroStrategy sells a share of MSTR, it can acquire approximately 98% of Bitcoin.

This means the company can use funds greater than the net asset value of Bitcoin to increase its Bitcoin holdings, thereby expanding its Bitcoin balance sheet. The core of this strategy is that MSTR can enhance the speed and scale of its Bitcoin holdings through high premium financing, significantly outpacing the previous speed of “debt-to-buy-crypto.”

Once this flywheel is in motion, MSTR’s increasing market value will also attract it to be included in U.S. stock indices, bringing in more incremental funds that generate additional asset net value premiums. One reason MSTR decoupled from BTC in the third quarter was that the market was anticipating its inclusion in the Nasdaq 100 index, which would result in substantial passive inflows.

U.S. index investors will be “forced” to invest in MicroStrategy, returning to the reflexive flywheel, which creates larger asset net value premiums, enabling MSTR to raise more funds to increase Bitcoin holdings, pushing Bitcoin prices up, enhancing market optimism for MSTR. The company’s weight in the index may increase, leading to further buying demands from index funds, creating a self-reinforcing positive feedback loop, resulting in a pressure flywheel for index buying.

From a broader time perspective, the amount of BTC that each MSTR share holder equivalently holds is continually increasing. This not only elevates market recognition of MSTR as a “Bitcoin alternative investment tool” but also enhances pricing expectations for MSTR.

“More MSTR in U.S. Stocks”

In recent weeks, MicroStrategy CEO Michael Saylor has become increasingly vocal, proclaiming on major podcasts and news programs that “there will be more MSTR in U.S. stocks” and that “MSTR’s mechanism is simply ‘infinite financial silver printing malfunction.'”

Saylor believes that MSTR’s “reflexive flywheel” model possesses powerful capital operation potential, enabling it to continuously accumulate Bitcoin while maintaining growth through financing and rising stock prices, demonstrating how a public company can leverage asset premiums and capital market financing capabilities for long-term expansion.

This model is not merely a traditional “buy and hold” strategy but an active approach to utilizing capital market advantages to expand its balance sheet. This mechanism could become a template for other companies, particularly in resource-intensive or capital-intensive industries. In fact, many companies have emerged that mimic MSTR’s partial asset operations.

Currently, this seemingly paradoxical model appears to be working well; according to recent data, for every $2.713 of stock issued, MSTR spends only $1 to purchase Bitcoin. Many believe that he is leveraging to long Bitcoin to outperform it significantly, but in reality, MSTR is in a healthy position; estimates suggest that it faces liquidation risk only if Bitcoin prices fall below $700.

For now, this mechanism seems to be functioning effectively, with MSTR continuing to increase its BTC holdings. However, as this mechanism becomes more widely adopted, it will undoubtedly lead to greater influence of crypto assets and related derivatives on U.S. stock indices, binding the cryptocurrency market and the U.S. stock market together and inducing profound changes in the market. For the cryptocurrency market, this introduces significant liquidity from U.S. stock funds (mainly absorbed by BTC), while for the U.S. stock market, it seems to amplify volatility risks.

According to Saylor’s vision, by 2050, Bitcoin’s price will reach $500,000 per coin, and he hopes that by then, MSTR will become a trillion-dollar company, better facilitating the deeper integration of cryptocurrency into people’s lives. Whether this seemingly “perfect version of a Ponzi scheme” can function until then remains to be seen by future markets.

-

-

-

-

-

-

-

-